Portfolio Rebalance / June 28

Following the Signal Sigma Process

The approach to this article follows the step by step process described here. All visuals are sourced from various instruments available in the platform. If you are using the Portfolio Tracker, you’ll be able to see how we set it up for our own portfolio at the end of this article.

We have delayed this week’s portfolio rebalancing process until the key trading day of the week, which is today. Asset markets have traded in a waiting pattern for the past couple of sessions, with today’s Core PCE data prone to move prices more meaningfully.

As it turns out, the Federal Reserve’s preferred gauge to measure underlying inflation, edged higher by 0.1% from the previous month. It was the softest increase since November of 2023, slowing from 0.3% in the three prior months. Meanwhile, the headline gauge refrained from increasing for the first time this year. On an annual basis, core PCE inflation slowed to 2.6% in May from 2.8% in the previous period.

The equity market’s reaction to the data was pleasing so far, with stocks rising. Bonds, however are tanking, with yields rising across the equity curve.

Asset Class Allocation

The first step in determining optimal portfolio positioning is taking a look at the performance of the main asset classes, and determining which are suitable for investment. The Asset Class Overview Instrument gives us a clear macro picture.

All asset classes remain investible this week.

SPY has maintained a bullish short and medium term technical composure, with immediate support at R1 and the 20-DMA managing to hold at every instance where there was even the slightest drawdown. While officially “overbought” with a score of 92/100, this is how equities behave in bull markets.

As noted in today’s Daily Briefing, many analysts have had to ratchet up their year-end price targets for the S&P 500. Goldman Sachs recently upped its price target to S&P 6300 for the end of this year, along with Evercore ISI upping its year-end target to 6000. In the absence of these upgrades, the market would seem prohibitively expensive, with relatively little fundamental upside.

Commodities (DBC) are squaring up to a heavy resistance cluster in the $23.4 area, where 3 key technical levels converge: the 50 and 200 DMAs, as well as the S2 retracement. A breakout would be incredibly bullish for commodities here, although it has to be said that oil (USO) was the main support factor for the whole commodity complex. Nat Gas (UNG) has also consolidated and held support at the 50-DMA.

Gold’s (GLD) support level has moved higher than the last close, as bullion has struggled to meaningfully continue its bull run. There is a potential “head and shoulders” pattern forming, which would be problematic if a break to the downside is realized.

TLT continues its consolidation in what is an increasingly bullish environment for treasuries given the lower inflation environment.

Enterprise, our core investment strategy, has kept the same allocation form the previous week, with minimal adjustments.

Stocks exposure via SPY is maintained at 69% this week.

Bonds exposure (IEF) is maintained at 25.3%.

The position in GLD is maintained at around 3%.

The position in DBC is maintained, at 1.2%.

The cash position is now just slightly higher, at 1.67%.

Since this model only trades 4 ETFs, we use it to judge overall portfolio positioning. The strategy’s risk profile is now “balanced”. We agree that this is the best way to go for now, as the risk reward skews in favor of treasuries rather than equities, for multiple reasons.

2. Sector / Industry Selection

The next step in creating our portfolio positioning is to break down each broad asset class into more granular groups of assets. This will help us understand which pocket of the market is outperforming or underperforming and make our selection accordingly.

Since Equities are an investible asset class, we’ll take a look at how different Factors are performing and check for any notable opportunities.

We have included tables for this week and the prior 3 article editions in order to help you compare developments (click on the arrows or thumbnails to cycle through the tables).

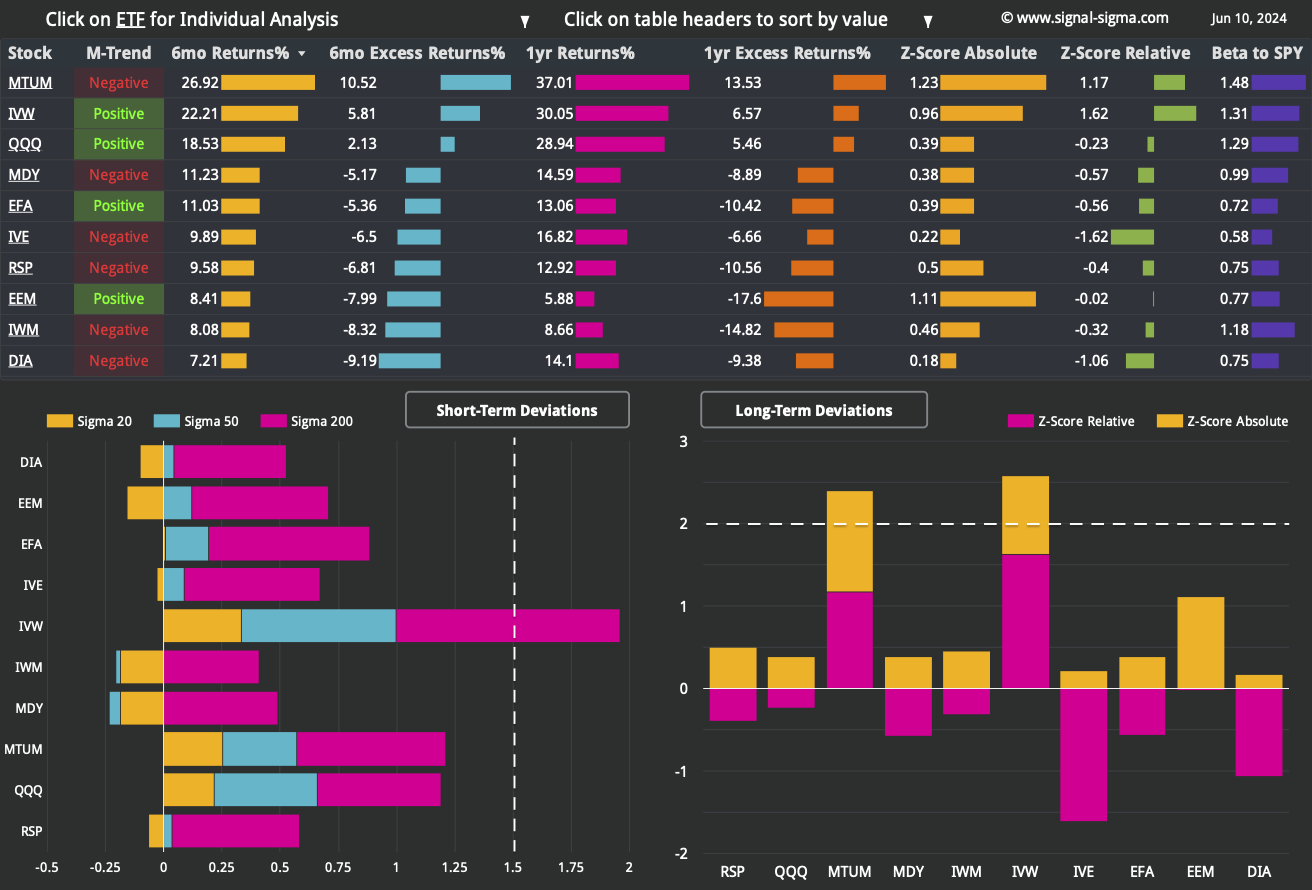

We’re just wrapping up the first half of 2024, so it’s worthwhile to check the 6 month return column. As it turns out, the only standout factors are Momentum Factor ETF (MTUM), Growth Stocks (IVW) and Nasdaq (QQQ). All of the rest have meager returns, with small caps actually posting a slightly negative performance.

In the short term, only Growth Stocks (IVW) are grossly overbought, with the Equally Weighted S&P500 (RSP) and Foreign Developed Markets (EFA) standing out as losers. In our opinion, small caps (IWM) are the factor to watch, as their direction is most telling for the breadth and health of the equity market rally. Currently, IWM is under some degree of pressure and completing a consolidation pattern.

Longer term, the only factors outperforming SPY are Momentum Factor ETF (MTUM) and Growth Stocks (IVW), both overbought to various extents.

Among more granular Factor Returns, high growth, expensive stocks are all the rage again. A high R&D to Gross Profit ratio is the number 1 factor correlated with top performing stocks all the way to the 6 month historical window.

Longer term (and across all timeframes as well), there are no factors that stand out. We have checked for the prevalence of expensive stocks via the Price to Sales metric, but that only comes up as a top factor sporadically across time frames.

Here’s how we stand on the Sectors front:

We have included 3 former tables from previous articles, for your convenience.

Looking at the sectors ETF leaderboard, we can quickly tell that none of them are extremely overbought or oversold in the short term. Tech (XLK), Communications (XLC) and Consumer Discretionary (XLY) are clearly leading, but they are not yet extended above moving averages.

Utilities (XLU) stood out for the fact that profit taking hit the otherwise rebounding sector. Chart-wise, we are noticing a level break after an outstanding run. There is plenty of downside for Utilities, but this is one dip that we are looking to buy.

The outstanding relative weakness of Industrials (XLI) versus SPY is still staggering. While the sector is holding its own support on an absolute basis, the relative chart is plumbing 2 year lows. Normally, a reversal should occur in the following month. Absent that, we may need to reduce exposure to the sector.

Nostromo maintains a risk-on allocation to equities via SPY and XLB (Basic Materials) ETFs, same as last week.

Bonds exposure is maintained via TLT, at a 21% weight.

Cash is sitting at -32%, as the strategy is leveraged especially toward equities. If XLB generates a SELL signal, the position will be closed out and cash levels will return to normal.

Finally, this model is starting to show some signs of life, at least on a 3-month horizon.

While underperforming in real life, this quirky model has its uses as a decision support tool. Nostromo has missed out on the rally since the October 2023 lows mainly due to its reliance on “trade signals” and lack of a minimal constant allocation quota. Nevertheless, it’s also illustrative to understand why underperformance can also stem from under-allocation and “waiting for the right time to invest”. If that time never comes, the opportunity cost is hard to make up. The system is actively trying to do that via utilizing leverage at this point.

3. Individual Stock Selection

Millennium Alpha is going through its own period of consolidation, as its underlying positions are heavily correlated with the Momentum Factor ETF (MTUM). Periods of weak relative performance are part and parcel of investing in any strategy.

The fact that many positions are also majorly correlated with Industrials (XLI) also did not help, since XLI is the sector with the largest relative-to-SPY underperformance deviation. As the next rebalance occurs, we’ll probably get a more balanced equity mix.

As per usual, you can tweak Millennium Alpha’s selection system using your own inputs if you wish.

4. Market Environment

The next step in our process is to take into account the type of market environment that we are currently trading in. For these purposes we use the Market Internals and the Market Fundamentals Instruments. Comments on the overall state of the market can usually be found in our Weekly Preview Article.

There’s been no improvement in market breadth in the past week. There’s been no deterioration either. Overall, the situation remains bad. Given enough time with no breakdown, this could transition into a positive catalyst - a resilient market with plenty of stocks ready to advance again. For now, we’re reading this as bearish.

Bearish Signal in Stocks trading above their 200-day Moving Averages

As a contrarian indicator, sentiment works best near extremes. And right now, we are trading very much near the middle of the 2-year range. If we use technical analysis on this series, we can clearly make out a wedge pattern that is going to break out or down sooner or later. For now, this reading is exceptionally close to neutral and has been for a while.

Neutral Signal in Sentiment

The comparison of Z-Scores reveals the disparity between large cap performance (SPY) and the top 1000 stocks by dollar volume (the broad market), equally weighted.

While the gap has closed a bit during the past week, the Z-Score divergence still remains on the ascent. We’ll need to see a much more pronounced pickup in performance for small caps in order to reverse this trend.

Bearish Signal in Market Internals Z-Score

Dollar Transaction Volume has surged in the past week, during the very slight dip. We’ll interpret this as a lot of buying interest clamouring to buy any available discount in the stock market. This is bullish, and we’ll upgrade this liquidity indicator accordingly.

Bullish Signal in Dollar Transaction Volume

5. Trading in the Sigma Portfolio (Live)

After reviewing all of the above factors, it’s time to decide on the actual investing strategy for our real-life portfolio.

The standout trade idea from this week’s market review is monitoring Industrials (XLI) and Utilities (XLU). If Industrials don’t bounce soon, we’ll be forced to start cutting exposure to that sector and start rotating into Utilities, which are currently hit by profit taking.

The growth oriented positions are doing fine, and for the moment there’s no need to pivot the asset class exposure of our live portfolio in any meaningful way. There is one position currently violating our stop-loss (POWL), so we’ll cut that and replace it with the technically excellent SPDR S&P Regional Banking ETF (KRE).

Automated Strategies and Market Outlooks

The Sigma Portfolio (Live)

As mentioned in the intro, the position in POWL has violated its stop-loss, so we need to cut it. We will replace its exposure with the SPDR S&P Regional Banking ETF. The overall asset class allocation of our portfolio will not change.

The following orders will be executed at today’s close:

We have also adjusted plenty of target and stop loss prices within our portfolio tracker, so as to reflect the latest technical backdrop of various stocks.

Click here to access our own tracker for the Sigma Portfolio and understand how the positions contribute to the overall exposure profile. Due to today’s adjustments, the risk-reward profile has been improved. Both stops and profit targets are now higher and offer a better risk-reward proposition.

In total, we stand to gain $17.456 by risking $10.890 if our targets are correct.

In terms of Factor correlations, exposure well balanced. This is insulating our portfolio from aggressive profit taking in Nasdaq (QQQ) and Momentum (MTUM) names - but has also led to a bit of underperformance lately. A balanced portfolio has not performed well in 2024 in comparison to SPY at least.

Looking at sectors correlations, we can see how a rotation strategy can benefit Utilities (XLU), since it is the sector we are least exposed to. The high Industrials (XLI) correlation is a bit concerning in the medium term, due to the relative-to-SPY underperformance. This potential defensive shift also makes sense from August onward, when a lower beta portfolio is preferred for the run up to the November elections.

If you have any questions, please contact us using your favorite channel. Have a great week everyone, and happy investing!

Andrei Sota