Portfolio Rebalance / November 13

Following the Signal Sigma Process

The approach to this article follows the step by step process described here. All visuals are sourced from various instruments available in the platform. If you are using the Portfolio Tracker, you’ll be able to see how we set it up for our own portfolio at the end of this article.

As the U.S. Elections have come and gone, and the Fed is still on track to lower interest rates, much fear has been removed from the market, as some risks have simply not materialized. The biggest gainers post elections have been recorded in small caps, financial stocks and cryptos, while big tech has been a relative under-performer.

The market has been volatile when it comes to interest rates. On one hand, yields have risen in the immediate aftermath of the elections, suggesting Trump’s policies are viewed as highly inflationary. On the other hand, gold and oil have sold off almost -7% since November 5’th. Both trades are not suggestive of higher inflation down the line, as both commodities are viewed as closely linked to inflation.

Basically, we’ve seen lower prices for everything except stocks and cryptos. According to a BofA analysis posted on Bloomberg, high-beta stocks tend to outperform in the final stretch of the year:

In fact, it’s a trend that plays out year in, year out. Bank of America notes that stocks with the highest volatility, known as beta, have tended to beat the market in the final two months, in part thanks to investors diving into high-octane shares in a bid to juice their performance. Funds tracked by BofA have been particularly allergic to risk taking this election season so far, suggesting there’s even more pressure this time round for investment managers to get bullish.

Moreover, around $6 billion of daily corporate share buybacks are due to hit the market, putting a clear floor under equities for the time being. The bullish setup remains firmly intact into early March, as noted by The MarketEar:

Here’s our investing process given the current state of affairs:

Asset Class Allocation

The first step in determining optimal portfolio positioning is taking a look at the performance of the main asset classes, and determining which are suitable for investment. The Asset Class Overview Instrument gives us a clear macro picture.

Equities and Gold remain investible this week; Treasuries and Commodities are non-investible;

SPY is currently back to overbought levels, but both the short and medium term trend continue to show a bullish bias at the moment. There is no reason to become bearish equities at the current juncture, with support close by, at $580.

Commodities (DBC) have fallen below the level that allows investment in our analysis process. The main weakness is found in oil prices, which have slipped despite fears of rising inflation. This is more of a reaction to a possible supply / demand imbalance coming as a result of Trump’s policies that encourage drilling. Demand in China is also not showing signs of revival just yet, so it’s no wonder that prices are falling for commodities.

Gold (GLD) retraced around -7% from recent all time highs, and narrowly lost the lead of the best performing asset class of the year as a consequence. The main impediment to Gold’s continued rise is two-fold. First of all: profit taking after a monster run in the past 2 years, and strength in the U.S. Dollar.

Our view is that Gold is an asset class to accumulate on significant dips, as demand is being stoked by foreign central banks which are dumping treasury bonds in favor of bullion. Read: the PBOC (China’s Central Bank) needs a backup asset in case the US decides to impose sanctions and freeze treasury reserves for whatever reason. The drawdown in Gold is now at -2 standard deviations.

TLT has closed a hair below our designated stop-loss level, and the asset class is non-investible at the moment as a consequence. While the margin is very thin (it seems like TLT is sitting right on support), we can’t really argue with the realities of inflation expectations and the impact of Trump’s future policies.

Long story short, TLT needs to rally by the end of the week. Today’s inflation figures have been reported right in line with expectations, but both headline and Core CPI inflation are now higher than they were 2 months ago. Needless to say, this is the wrong direction and the Fed will have a tough job navigating the current environment.

Enterprise, our core investment strategy is doing what other asset managers have been busy doing and is re-risking. Almost the whole allocation is tilted toward equities, as bond exposure is not allowed according to our rules.

Stocks exposure via SPY has been increased from 39% last week to 82% today.

Bonds exposure (IEF) has been completely removed.

The position in GLD remains small, at about 3.3%.

Commodities (DBC) are also deemed un-investible, so the position is being closed.

Since this model only trades 4 ETFs, we use it to judge overall portfolio positioning. Enterprise is now risk-on and almost all-in on stocks. Given the current set-up, this is probably the best stance.

2. Sector / Industry Selection

The next step in creating our portfolio positioning is to break down each broad asset class into more granular groups of assets. This will help us understand which pocket of the market is outperforming or underperforming and make our selection accordingly.

Since Equities are an investible asset class, we’ll take a look at how different Factors are performing and check for any notable opportunities.

We have included tables for this week and the prior 3 article editions in order to help you compare developments (click on the arrows or thumbnails to cycle through the tables).

Winners and losers after the elections are starting to become clear from a Factors perspective. The biggest losers by far have been Foreign Developed Markets (EFA), as European stocks have severely under-performed. The market is sending a clear message: “America First” means “everyone else last”. Stunning.

On the other hand, the winners are all domestically focused companies. The iShares Russell 2000 ETF (IWM) jumped way above its normal trading channel in an equally stunning breakout. We believe these knee jerk reactions are set to continue in the months and even years ahead.

Among more granular Factor Returns, companies with higher debt loads have performed very well. This is counter-intuitive when considering a spike in yields. The main explanation is found in the regional banks space (highly indebted), but which have also skyrocketed +15% since the election due to deregulation optimism.

Across all timeframes, a new factor has emerged - the quite bland sounding “Assets Growth”. Investors prefer companies which grow their assets base? Who would have thought? Seems like a no-brainer, in retrospective.

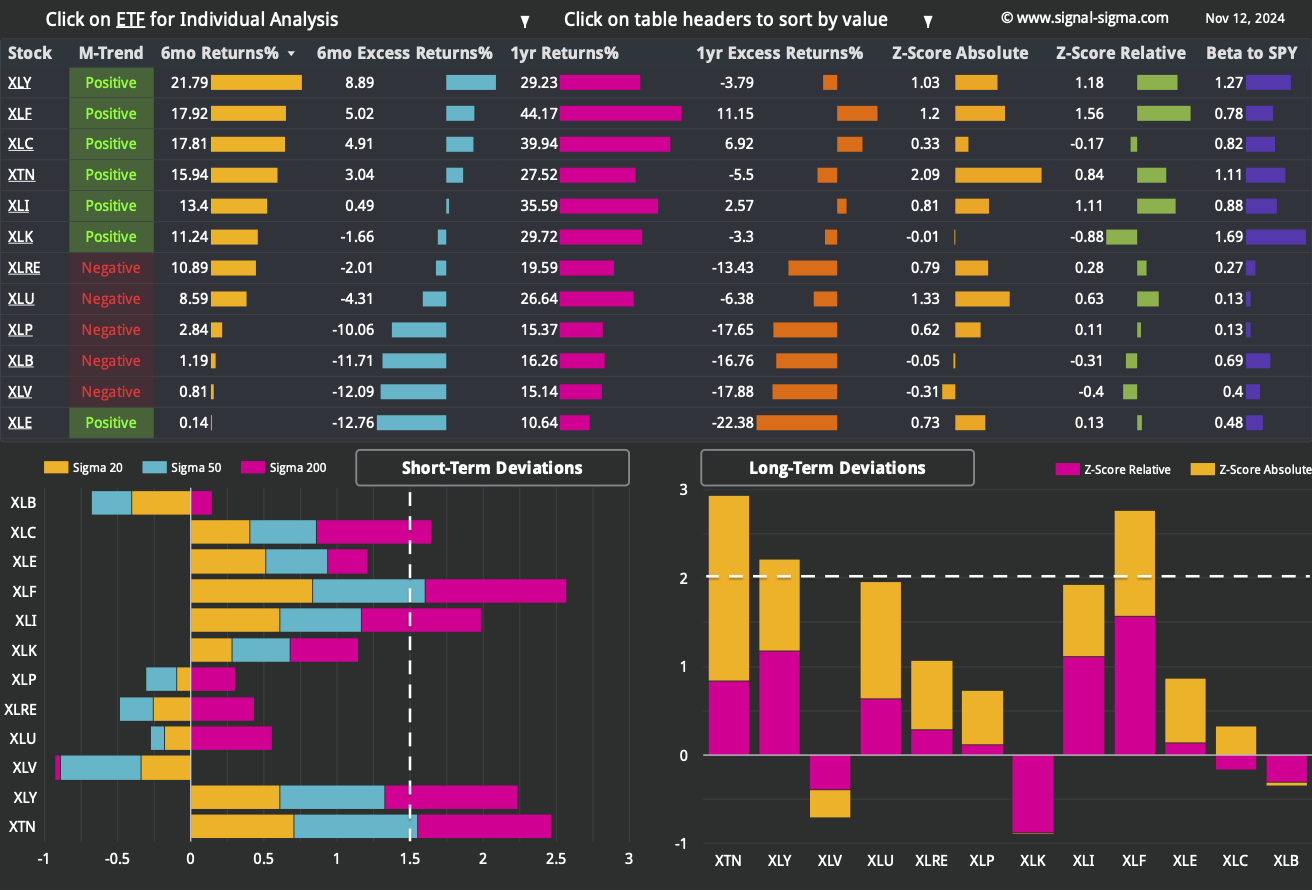

Here’s how we stand from a Sectors standpoint:

We have included 3 former tables from previous articles, for your convenience.

As was the case with Factors, the Sectors leaderboard tells a similar story in the sense that we can distinguish between the winners and losers.

Healthcare (XLV) is presumably the worst off sector, as pharma companies are probably not very excited at the perspective to work with RFK Junior to “Make America Healthy Again”. The other defensive sectors like Staples (XLP), Real Estate (XLRE), and Utilities (XLU) have also under-performed post election.

Financials (XLF), Consumer Discretionary (XLY) and Transports (XTN — also closely linked to the discretionary portion of the economy) are now recording high extensions in the short term. Curiously, Tech (XLK) is a relative-to-SPY under-performer, despite the fact that it’s doing well in absolute terms.

Industrials (XLI) are also set to benefit from domestically focused initiatives, and have performed well in the past week.

We believe these trends are here to stay and can’t be faded to a large extent. Sure, pullbacks are always expected form extreme values, but we would expect these themes to dominate in the next couple of months.

Nostromo, our quirky tactical allocation model, is buying the dip in Staples (XLP), adding a hefty 54% position.

While the trade makes sense on a purely technical perspective (XLP is a relative out-performer and just had a significant drawdown), we wouldn’t dedicate half of our portfolio to it.

Nostromo is also holding a significant position in bonds, via a combination of TLT and MBB (Mortgage Backed Securities) and only 19% in cash. The overall exposure profile is risky enough to tell us that the rally is set to continue and Nostromo is betting on a rotation ahead.

3. Individual Stock Selection

Millennium Alpha is still going strong, especially as the post election rally has favored certain stocks in this portfolio. The jump in performance was staggering and left some of our clients in shock at the amount of money shown in their portfolios.

Some of the recent winners here include APP (now doubling since inception) and POWL, but it’s not like the other picks have done badly either. Millennium Alpha is geared toward Momentum (MTUM) and Growth (IVW) stocks on the factors side and Tech (XLK) + Industrials (XLI) on the sectors side.

For this week, the system has only bought positions back to target weights. Next week, a full rebalancing and refresh will occur, and we look forward to the trades that this strategy will execute -- some notable changes are bound to happen given the shifting landscape.

4. Market Environment

The next step in our process is to take into account the type of market environment that we are currently trading in. For these purposes we use the Market Internals and the Market Fundamentals Instruments. Comments on the overall state of the market can usually be found in our Weekly Preview Article.

We are trading in a healthy market breadth environment, with a majority of stocks priced above their respective 20, 50 and 200 moving averages. This environment is conductive to a sustained rally, without showing signs of “overheating”.

Bullish Signal in Stocks trading above their 200-day Moving Averages

As a contrarian indicator, sentiment works best near extremes. The current reading (58/100) is borderline in “Greed” territory, but not quite.

Despite calls of the market being “euphoric”, the evidence currently does not support such a view. There have been times in the past where enthusiasm had been much higher than current levels. We would call the current sentiment “optimistic”, but not more than that. Investors are aware stocks are near all-time highs, valuations are expensive by almost any metric, so there are reasons to keep cash on the sidelines.

This is not the time to take a contrarian view and bet against this market.

Neutral Signal in Sentiment

The comparison of Z-Scores reveals the disparity between large cap performance (SPY) and the top 1000 stocks by dollar volume (the broad market), equally weighted.

The performance of small and mid cap stocks has been on par with that of SPY, when adjusted for volatility. The fact that these two parts of the market are trading in tandem is a bullish indicator, as it shows the bulk of stocks are resilient to shocks. It is curious to observe that the Z-Score Divergence is not higher in favor of small and mid-caps, however. This is owing to the fact that Z-Score is a reading that adjusts for expected volatility.

Bullish Signal in Market Internals Z-Score

Dollar Transaction Volume went through the roof during the past week and reached record values. Given that the market has also surged, the increase in volume is indeed extremely bullish. It is telling of the fact that many investors needed to re-allocate towards risk, and our interpretation is that flows will continue to support a further rally.

Very Bullish Signal in Dollar Transaction Volume

5. Trading in the Sigma Portfolio (Live)

After reviewing all of the above factors, it’s time to decide on the actual investing strategy for our real-life portfolio.

We have identified a couple of themes so far:

Bonds and Commodities are trades which we need to lighten up on;

There could be an opportunity to buy Gold and Staples (XLP) on the dip;

The momentum trade is in Small Caps (IWM), especially Industrials (XLI) and Financials (XLF) sectors of the market

We will perform our portfolio rebalancing following these themes, as risk exposure overall needs to be maintained.

Automated Strategies and Market Outlooks

The Sigma Portfolio (Live)

First thing’s first. We need to remove positions that are underperforming / not working as expected. These are dragging on our performance and we need to reduce or cut them completely. The big elephant in the room is the position in TLT, at 40% weight (this is because the Sigma Portfolio is benchmarked to a 60-40 stocks-bonds portfolio). We’ll begin by starting to trim this:

SELL 10% TLT (Reduce position to 30%)

Next, we will also cut the only remaining position with Energy (XLE) exposure:

SELL FANG (Close Position)

We will add to Gold on the dip and add to a couple of our existing positions:

BUY 5% GLD (Initiate 5% Position)

BUY 2% POWL (Add 2% to Position)

BUY 1% FTDR (Add 1% to Position)

BUY 1% CL (Add 1% to Position)

BUY 2% IESC (Initiate 2% Position)

All of these trades will be executed at tomorrow’s close (Thursday, November 14).

Click here to access our own tracker for the Sigma Portfolio and review how each position contributes to the overall exposure profile. We have recently updated all price targets and stop targets to reflect ongoing developments.

In total, we stand to gain $26.309 by risking $13.103 if our targets are correct. The risk-reward equation continues to remain favorable, with a nearly 2-1 ratio.

Among sectors, we are underweighting defensive sectors (XLU, XLP, XLRE) in favor of Tech (XLK), Industrials (XLI), Communications (XLC) and Consumer Discretionary (XLY).

If you have any questions, please contact us using your favorite channel. Have a great week everyone, and happy investing!

Andrei Sota