Portfolio Rebalance / November 20

Following the Signal Sigma Process

The approach to this article follows the step by step process described here. All visuals are sourced from various instruments available in the platform. If you are using the Portfolio Tracker, you’ll be able to see how we set it up for our own portfolio at the end of this article.

Last week we made some notable changes in our live portfolio, as we continue to navigate the still volatile post-election climate. The bullish bias in risk assets remains intact for now, as analysts and economists get more optimistic on the future.

Just during the last days, well known economist Ed Yardeni raised his target for the S&P 500, lifting his call to 10,000 for the close of the decade (from 8.000 earlier). His estimates call for the S&P 500 to end 2024 at 6100, reach 7000 in 2025, 8000 in 2026, and 10,000 in 2029. This implies a ~7% CAGR for the next 5 years, in line with historical returns, but much lower than the market’s current 21% CAGR (on a 2 year basis).

Even Mike Wilson from Morgan Stanley, famous for his unrealized bearish calls, has flipped bullish. Mike now has a best-case-scenario of 7.400 for the end of 2025, even higher than Yardeni’s. From current prices, the upside could reach +25% for an ETF like SPY.

While equities get these optimistic takes, more speculative assets (non-profitable tech, crypto and meme stocks) are continuing their explosive run. Safe havens have been dumped. TLT, the benchmark treasury ETF has had its largest outflow since 2020.

CTAs are heavily short treasury bonds which has historically been a good time to be contrarian and long, as they scramble to cover on yield declines.

Even Gold, and especially Gold Miners (GDX) had just had a sizable drawdown (near 2 standard deviations).

In light of what’s working and what’s not, we’ll start our step-by-step Portfolio Review and weekly Rebalancing process.

Asset Class Allocation

The first step in determining optimal portfolio positioning is taking a look at the performance of the main asset classes, and determining which are suitable for investment. The Asset Class Overview Instrument gives us a clear macro picture.

All asset classes are now investible again;

SPY is trading on the low side of its immediate term risk range, with the 50-DMA and M-Trend levels close by and offering support. The benchmark equities ETF is no longer technically overbought (71/100) and its short term MACD has flipped negative. Supply and demand dynamics should still favor the bulls into year end, but for the moment some sloppy trading is expected, as investors re-calibrate following Trump’s election win — the initial short covering surge higher is now partially retracing.

Commodities (DBC) have flipped on the positive side of our stop-loss level yet again — mainly on geopolitical catalysts. This is a tough asset class to trade at the moment, as it’s experiencing a transition to a range-trading environment. For the moment, the old Wall Street adage seems adequate: “If in doubt, stay out.”

Gold (GLD) has found a temporary bottom near M-Trend support, also bouncing on geopolitical concerns and benefiting from its safe-haven status. Gold has seen its fair share of speculative fervor this year, as it’s still the best performing major asset class in 2024.

The recent -8% drawdown was entirely predictable, purely as a function of profit taking. But gold’s fundamentals are strong, especially as the price is well supported by central bank buying. We own a small position in GLD and plan to add Gold Miners (GDX) on this dip.

In 2023, GDX had a double bottom before a 20+% rally pushed it above the prior peak. The current discount makes this a technically good setup for both Gold and Gold Miners.

TLT has closed a hair above our stop loss level at $90.4 and is technically investible at this point. As a contrarian play, we favor bonds, and the plan was to keep selling down our position in TLT if it kept trading below its stop loss level. However, that’s not the case today. We’ll keep a close eye on bonds going forward, as treasuries remain an excellent hedge in the event of a slower economy.

Enterprise, our core investment strategy is maintaining a very similar asset allocation from last week.

Stocks exposure via SPY has been incrementally increased from 82% last week to 83% today.

Bonds exposure (IEF) continues to be 0%.

The position in GLD remains small, at about 3.3%.

Commodities (DBC) make up around 1.5% of the portfolio.

Since this model only trades 4 ETFs, we use it to judge overall portfolio positioning. Enterprise is now almost fully risk-on. In the absence of treasuries exposure, the only other viable asset class are stocks, and that is reflected in the current allocation.

2. Sector / Industry Selection

The next step in creating our portfolio positioning is to break down each broad asset class into more granular groups of assets. This will help us understand which pocket of the market is outperforming or underperforming and make our selection accordingly.

Since Equities are an investible asset class, we’ll take a look at how different Factors are performing and check for any notable opportunities.

We have included tables for this week and the prior 3 article editions in order to help you compare developments (click on the arrows or thumbnails to cycle through the tables).

This week, the staggering underperformance of international stocks versus their US peers continues unabated. Since February this year, the Foreign Developed Markets ETF (EFA) is up just +2.5%, while a factor like US Growth (IVW) is up more than +20% in the same period. Unfortunately, this is not a buy-the-dip opportunity for EFA or EEM for that matter. If both of these ETFs are underperforming when markets are booming, how will they perform in more adverse conditions?

Other than the domestic versus international disparity, the Factors leaderboard looks broadly positive, with the best value in Nasdaq (QQQ) — still a relative under-performer.

The iShares Russell 2000 ETF (IWM) and Growth Stocks (IVW) are the only two ETFs outperforming SPY on a 6 month basis, and not by much. There are no tactical opportunities to speak of at the moment, but small caps should perform well in the year ahead as well.

Among more granular Factor Returns, companies with higher debt loads continue to perform very well. This is counter-intuitive when considering a spike in yields. The main explanation is found in the regional banks space (highly indebted), but which have also skyrocketed +11% since the election due to deregulation optimism.

Across all timeframes, a high R&D / Gross Profit has been heavily favored. These companies are usually hyper-growth focused and not especially profitable (that’s where the high ratio is derived from). In other words, speculative stocks are primed to make a comeback!

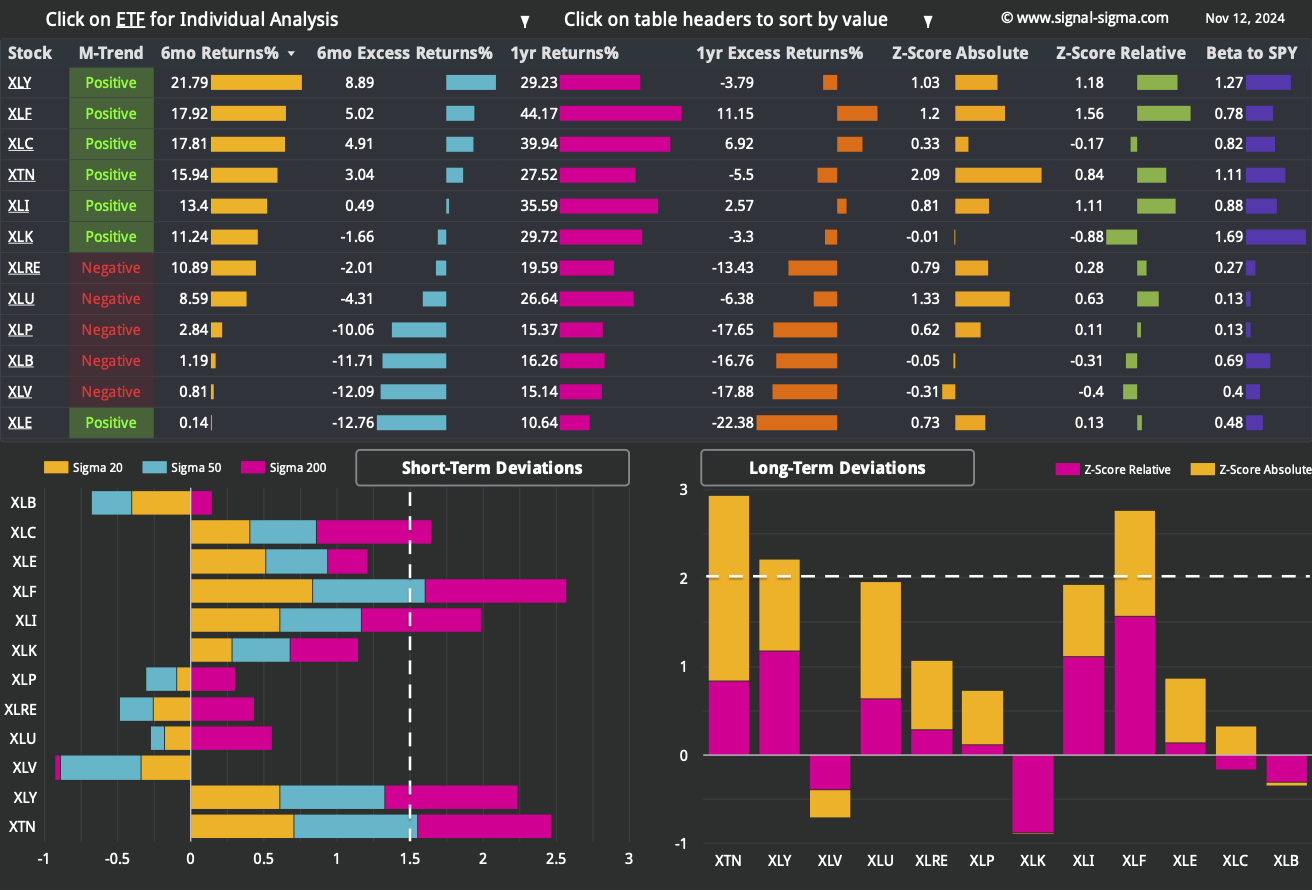

Here’s how we stand from a Sectors standpoint:

We have included 3 former tables from previous articles, for your convenience.

Among sectors, Healthcare (XLV) is under tremendous selling pressure in the short term, as pharma stocks have taken a major hit to share prices following Trump’s pick to lead the Health and Human Services department: Robert Kennedy Jr. This seems like a frivolous reason for a selloff of this magnitude, but if his proposals are enacted, then we agree it’s bad news for the sector. Technically speaking, at nearly -3 Sigma Score (where -3 is max negative), the price move is overdone, and we would expect a snap-back rally in the next period.

Healthcare aside, 6 sector ETFs are outperforming SPY over the last 6 months. This is excellent news in terms of market breadth! However, only 7/12 ETFs are trading in a medium term positive trend, meaning that momentum is not at all as positive as the headline price action would suggest at the index level.

Financials (XLF), Transports (XTN), and Consumer Discretionary (XLY) look extended at the moment and prone to some short term profit taking.

A tactical allocation can be initiated in Real Estate (XLRE) and Staples (XLP), since both of these sectors have retraced from all-time-highs near technical support, but are otherwise out-performers.

Nostromo, our quirky tactical allocation model, maintains a hefty 54% position in Staples (XLP), betting on a technical reversal.

It is also looking to acquire Emerging Markets (EEM) on a valid BUY signal, while the rest of the portfolio is targeting bonds.

On that note, today’s very small TIP trade (inflation protected bonds) works to fill the very diverse bonds portfolio that does not include TLT.

3. Individual Stock Selection

Millennium Alpha has just refreshed its portfolio yesterday. The portfolio refresh runs our stock picking algorithm in order to select the top 15 stocks in this strategy and occurs once every 4 weeks.

New positions in Millennium Alpha:

Vistra Energy Corp - VST

Allison Transmission Holdings Inc - ALSN

Kontoor Brands Inc - KTB

EMCOR Group Inc - EME

Deckers Outdoor Corporation - DECK

Closed positions:

Comfort Systems USA Inc - FIX

MercadoLibre Inc. - MELI

Coca-Cola Consolidated Inc. - COKE

Arista Networks - ANET

Trane Technologies plc - TT

Powell Industries Inc - POWL

Frontdoor Inc - FTDR

The rest of the positions have been scaled back to target weight. This month, the correlation to the Momentum Factor ETF (MTUM) is reduced, but remains primary, along with Growth Stocks (IVW). On the Sectors side, Tech (XLK) and Industrials (XLI) are the primary correlations of this portfolio.

After previously reaching a high watermark above 60% year-to-date, the model has posted quita a large drawdown, currently at -6%. This is one of the largest this year, so it may be a good buying opportunity into this strategy.

4. Market Environment

The next step in our process is to take into account the type of market environment that we are currently trading in. For these purposes we use the Market Internals and the Market Fundamentals Instruments. Comments on the overall state of the market can usually be found in our Weekly Preview Article.

Market breadth remains healthy, with a majority of stocks priced above their respective 20, 50 and 200 moving averages. This environment is conductive to a sustained rally, without showing signs of “overheating”.

Bullish Signal in Stocks trading above their 200-day Moving Averages

As a contrarian indicator, sentiment works best near extremes.

Despite whatever anyone else may argue, we are not seeing anywhere near “euphoric” levels of confidence, similar to other dates in the past. Sentiment is decidedly neutral at the moment.

Neutral Signal in Sentiment

The comparison of Z-Scores reveals the disparity between large cap performance (SPY) and the top 1000 stocks by dollar volume (the broad market), equally weighted.

As has been the case since mid-August, the performance of small and mid cap stocks has been on par with that of SPY, when adjusted for volatility. This is a bullish indicator, as it shows the bulk of stocks are resilient and trading in lockstep with large and mega-caps.

The breadth issue that was present at the start of the year (when the divergence was near records has been resolved, especially post election.

Bullish Signal in Market Internals Z-Score

Dollar Transaction Volume has tapered off a bit since last week, as excitement over the rally has faded somewhat. However, it remains stuck at very high levels, as flows into equities remain strong. This should facilitate dip-buying, as volatility gets compressed when liquidity is abundant.

Very Bullish Signal in Dollar Transaction Volume

5. Trading in the Sigma Portfolio (Live)

After reviewing all of the above factors, it’s time to decide on the actual investing strategy for our real-life portfolio.

We will maintain our overall risk-on allocation in the Sigma Portfolio and continue to make adjustments as needed. First of all, our position in Eli Lilly (LLY) has violated its stop-loss and should normally get cut. However, given the very high downside deviation for the whole Healthcare sector, we’ll give this one more week to bounce.

Our tactical play in the Regional Banks space has paid off nicely and we will take profits on KRE. We will replace this with another tactical position, buying Gold Miners (GDX) on this dip. Finally, we will replicate Millennium Alpha’s trades and replace POWL and ANET with ALSN and VST.

Automated Strategies and Market Outlooks

The Sigma Portfolio (Live)

To sum up, here are the orders for tomorrow’s market close:

SELL 100% of KRE (Close Position)

SELL 100% of POWL (Close Position)

SELL 100% of ANET (Close Position)

BUY 3% GDX (Initiate a 3% Position)

BUY 3% ALSN (Initiate a 3% Position)

BUY 3% VST (Initiate a 3% Position)

BUY 2% IESC (Add 2% to Position)

BUY 2% NFLX (Add 2% to Position)

All of these trades will be executed at tomorrow’s close (Thursday, November 21).

Click here to access our own tracker for the Sigma Portfolio and review how each position contributes to the overall exposure profile.

In total, we stand to gain $29.172 by risking $13.626 if our targets are correct. The risk-reward equation has improved courtesy of our latest rebalance.

Among sectors, we are underweighting defensive sectors (XLU, XLP, XLE) in favor of Tech (XLK), Industrials (XLI), Communications (XLC) and Consumer Discretionary (XLY).

If you have any questions, please contact us using your favorite channel. Have a great week everyone, and happy investing!

Andrei Sota