Portfolio Rebalance / October 09

Following the Signal Sigma Process

The approach to this article follows the step by step process described here. All visuals are sourced from various instruments available in the platform. If you are using the Portfolio Tracker, you’ll be able to see how we set it up for our own portfolio at the end of this article.

As we’ve discussed recently in our articles and Daily Briefings, the future of the equity market largely depends on the upcoming Q3 Earnings Season results and guidance. In the absence of stock-specific catalysts, investors have no choice but to examine various economic data points and try to infer the health of the economy. Critical is also the Fed’s reaction to these data points, as investors are looking for signals that activity has the right “temperature”.

Signals that are too cool spark recession worries. Hotter numbers create inflation problems. The Fed’s job is to “thread the needle” and achieve persistent low inflation, without triggering a recession. To that end, their approach was successful so far., with the latest inflation numbers due to be released tomorrow.

We regularly watch alternative data feeds in order to make better informed decisions around these key release dates. One such alternate inflation tracker is called Truflation, which has been accurate in predicting the trend of inflation using live daily spending data sets. While the overall trend this year is certainly tracking in the right direction (lower), there is a notable jump developing during the last month, coinciding with the increase in yields. Part of the move has already been priced in by the bond market.

Besides inflation, the Fed’s dual mandate concerns the labor market as well. On that note, last week’s employment report was not as great as it seemed. As has been the case since the end of the Covid crisis, various seasonal adjustments and revisions are creating real difficulty in analyzing the data beyond the headline numbers.

For instance, Arkomina Research points out that we’ve just had the biggest seasonal adjustment in the BLS survey history. Arkomina calculates that had last year’s seasonal adjustment been used, the payroll growth would have been in line with expectations at +145k, not +254k, as reported.

Government job growth was also scrutinized by ZeroHedge. The BLS reported that 785k jobs were added to the labor market by the government. However, on a non-adjusted basis, the increase in government jobs in September dwarfs prior September data.

Finally, average hours worked by employees are not rising, as typically occurs in a robust jobs market.

Given all of the above, it’s no wonder investors are hedging against potential downside using more indirect means (options on the VIX, tracked by VVIX). If you only had access to the VVIX data as shown below, you would be excused for thinking that the market was in the midst of a major corrective episode — and certainly not making fresh all time highs.

In conclusion: some things don’t jibe. That’s why we have our process to rely on.

Asset Class Allocation

The first step in determining optimal portfolio positioning is taking a look at the performance of the main asset classes, and determining which are suitable for investment. The Asset Class Overview Instrument gives us a clear macro picture.

All major asset classes are investible this week.

SPY has maintained the recent bullish trend intact, bouncing off support at the 20-DMA and M-trend level. The bias remains to the upside, as bulls continue to be in charge of the narrative.

Commodities (DBC) hit the top trendline of the trading channel and immediately retraced below key support (S1). The main catalyst was the movement of oil (USO), with traders reacting to geopolitical tensions in the Middle East. It remains to be seen whether this is a full reversal to the 50-DMA, or a pause before a further rally.

Gold (GLD) hit the upper trading channel trendline and promptly retraced a part of the recent gains. Higher yields generally put selling pressure on the price of gold, as the yellow metal can only appreciate in value and pays no coupon. Some profit taking is also normal at these levels. There is some marginal support at the 20-DMA just below the last close, but more meaningful support can be found at $237 (R1).

TLT stopped declining but remained in deep oversold territory in the medium term. The next major support level stands at $93, with the 200-Day moving average also close by. While this looks like a great time to add bonds to a portfolio, we would rather wait for a clear reversal signal before buying additional treasuries. Furthermore, tomorrow’s inflation print has a real possibility of surprising to the upside — not good for bond prices.

Enterprise, our core investment strategy, has kept its allocation broadly unchanged from last week, with the only notable addition of a small commodities position.

Stocks exposure via SPY is maintained at 70%.

Bonds exposure (IEF) is maintained at 25%.

The position in GLD has fractionately declined from 3% last week to 2.8% today.

Commodities have been re-added to the portfolio, as DBC became investible. The 1.24% position is not impactful overall.

Since this model only trades 4 ETFs, we use it to judge overall portfolio positioning. Enterprise shows a balanced but risk-friendly approach, with cash levels staying low (1.55%).

2. Sector / Industry Selection

The next step in creating our portfolio positioning is to break down each broad asset class into more granular groups of assets. This will help us understand which pocket of the market is outperforming or underperforming and make our selection accordingly.

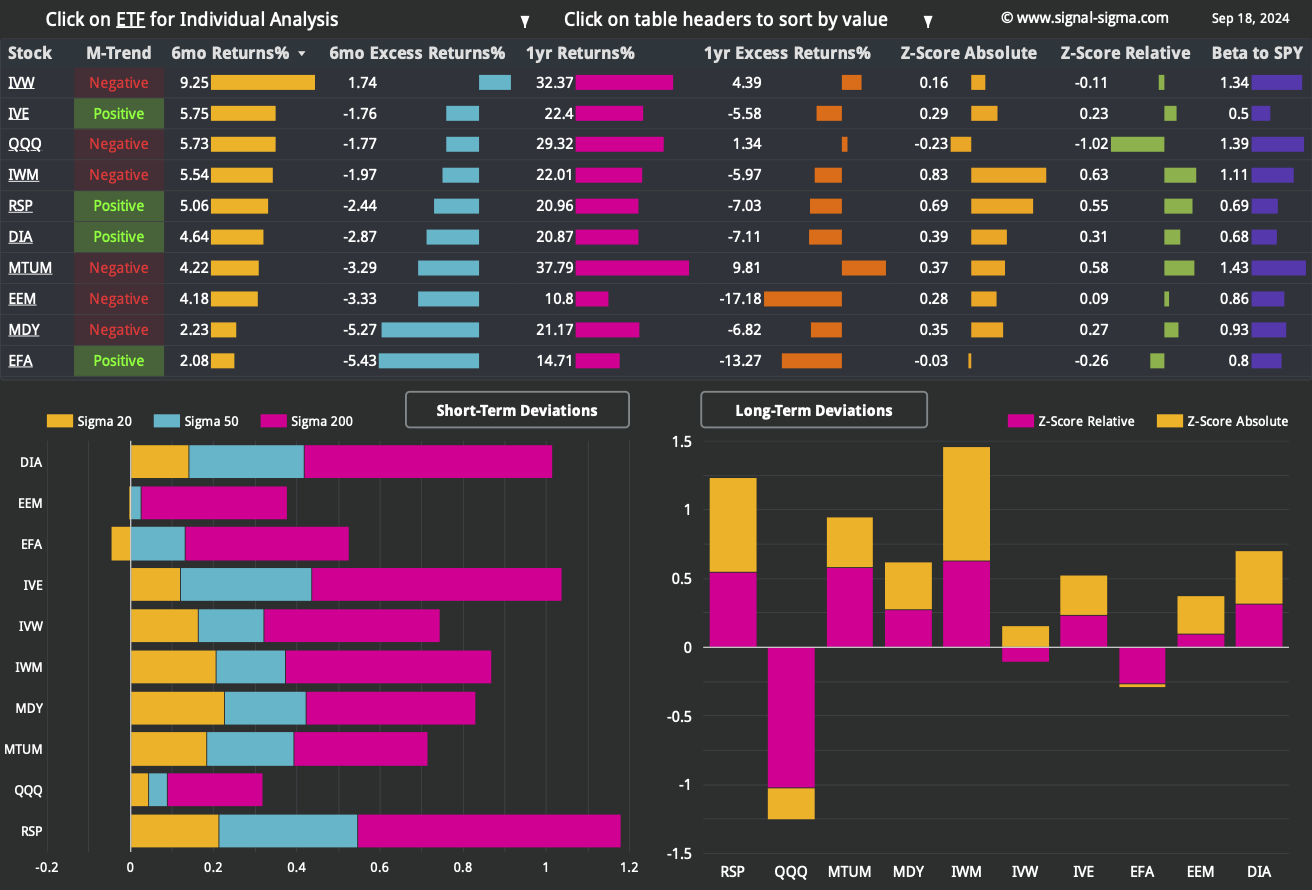

Since Equities are an investible asset class, we’ll take a look at how different Factors are performing and check for any notable opportunities.

We have included tables for this week and the prior 3 article editions in order to help you compare developments (click on the arrows or thumbnails to cycle through the tables).

The major difference from last week on the Factors leaderboard is the pullback in Emerging Markets (EEM). Chinese stocks (CSI 300) opened Tuesday morning following their week-long Golden Week holiday, with a massive +11% pop higher. However, shortly after opening, the index gave up half of the surge as China’s economic planning agency did not offer additional economic, monetary, or financial stimulus. Before Tuesday’s trading, the CSI 300 was up nearly 50% on the stimulus measures in just a few weeks. But the index gave up a third of its recent gains without new stimulus. While still overbought in the short term, EEM’s deviation is now closer to historical norms — not surprising since the price action was simply unsustainable.

Otherwise, factors paint a broadly bullish picture, although small caps (IWM), Foreign Developed Markets (EFA) and Value Stocks (IVE) have violated 20-DMA support. Besides EEM, there are no overbought or oversold factors in the short or long term. This is bullish in the context of all factors trading in a positive medium-term trend.

Among more granular Factor Returns, companies which heavily invest in new technologies have done very well, with the R&D / Gross Profit factor among the top of the short term timeframes.

In the longer term, companies with a high Assets Growth have stood out as winners, although the factor leaderboard is a bit “murky” — there is no clear dominating factor.

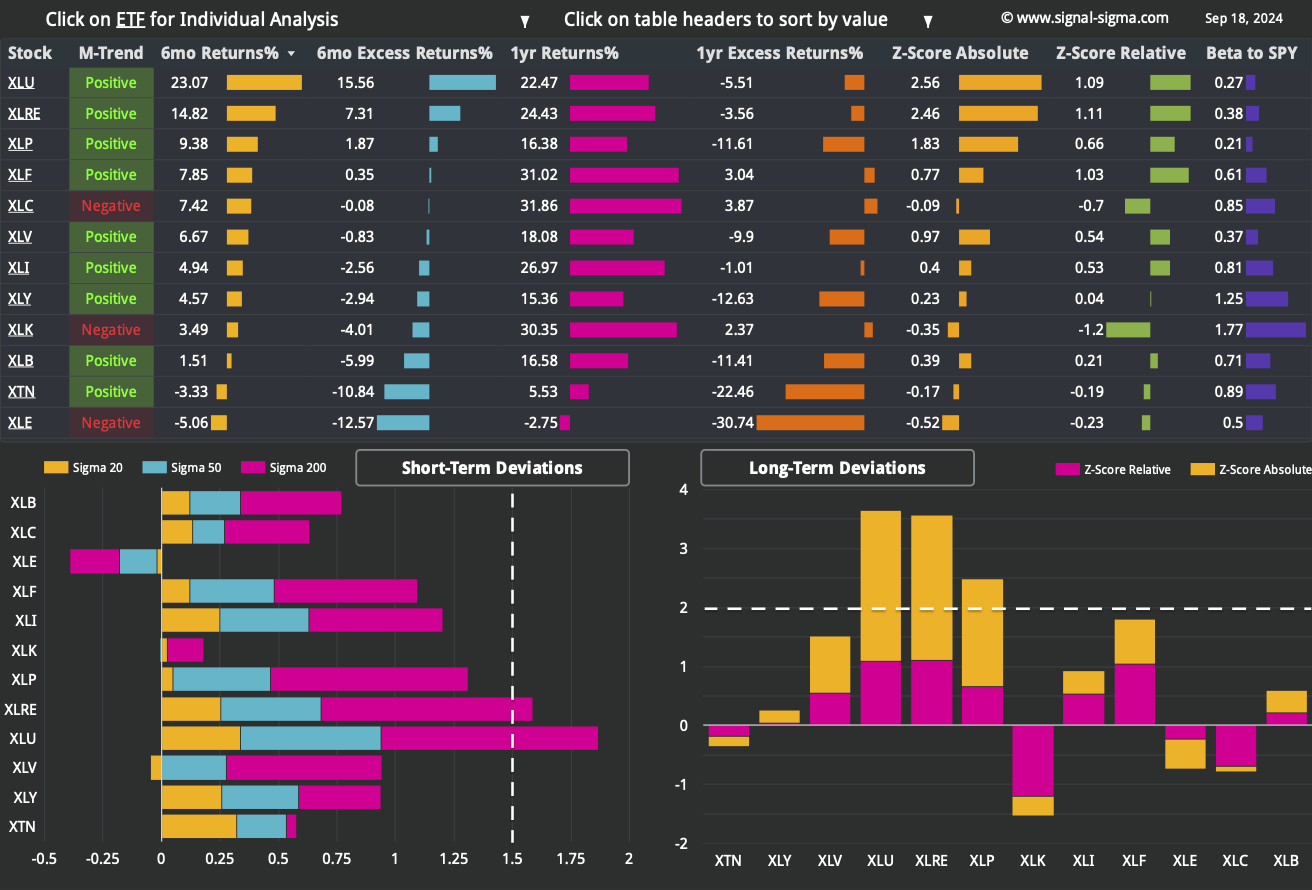

Here’s how we stand from a Sectors standpoint:

We have included 3 former tables from previous articles, for your convenience.

The Sectors dashboard also paints a bullish picture, similar to the Factors leaderboard. Interestingly, we find 3 out of the 4 the main defensive sectors in a negative medium-term trend — which is actually a positive factor. A “true” risk-on rally should not have leadership from Real Estate (XLRE), Staples (XLP) and Healthcare (XLV), for example.

Utilities (XLU) continue to perform exceedingly well, but we increasingly view Utility companies as third-order beneficiaries of the AI boom, by this logic: AI software <require> chips <which in turn require> data centers <which in turn require> lots of electricity <which needs to be delivered by> an expanded power grid.

All other sectors are trading in bullish trends and are not overbought in the short or longer term.

Tactical buy-the-dip opportunities are available in Healthcare (XLV) and Staples (XLP), as these two sectors are relative outperformers, but have both traded below their 50-DMAs recently. Given the proper reversal signal (patience with these!), allocation can commence, as both sectors are nearing oversold conditions in the medium term. Longer term, XLV looks fine, but XLP is still highly deviated.

After ripping higher +11% in the past 3 months and beating every benchmark, Nostromo maintains its flat exposure profile (the negative SPY position is negligible — basically a display artefact).

The model is targeting a tactical allocation in a couple of sector ETFs (the same that we have identified in the section above):

Each position will be initiated whenever a BUY signal is detected.

In addition to potentially acquiring these equity ETFs, Nostromo is also planning to initiate a treasury allocation using TLT.

In summary, Nostromo will remain flat until a tactical opportunity re-emerges either for stocks or bonds.

3. Individual Stock Selection

Millennium Alpha maintains the same portfolio composition as last week. Major Factor correlations include Momentum (MTUM) and Growth Stocks (IVW), while Tech (XLK) and Industrials (XLI) dominate on the Sectors side.

Speaking of which, our pure Momentum version of Millennium is doing very well recently, using completely different stock picks compared to Millennium Alpha. The model is on its way to close a very long 920 day drawdown period and establish a new high watermark, as performance starts to improve dramatically versus its benchmark. Stocks like ADMA Biologics Inc (ADMA) and Zeta Global Holdings Corp (ZETA) are currently its biggest winners, comparable to NVIDIA (NVDA) and Meta Platforms (META) in Millennium Alpha.

4. Market Environment

The next step in our process is to take into account the type of market environment that we are currently trading in. For these purposes we use the Market Internals and the Market Fundamentals Instruments. Comments on the overall state of the market can usually be found in our Weekly Preview Article.

Market breadth has not kept up with the recent advance, as we notice a decline in the number of stocks trading above their 20-DMAs. On one hand, this is indicative of a market that has slightly cooled off -- with some investors losing enthusiasm. On the other hand, levels for 50-DMAs and 200-DMAs remain healthy. In other words, this looks and feels like a normal consolidation in the broad market.

Bullish Signal in Stocks trading above their 200-day Moving Averages

As a contrarian indicator, sentiment works best near extremes. The current reading (59/100) is the last increment of “Neutral”.

Despite the market trading around all-time-highs, sentiment took a surprising turn lower recently. Under normal circumstances, we would have expected to see more exuberance in this metric. On one hand, sentiment more aligned with “Neutral” values is bullish, in the sense that it leaves “room” for further upside to develop. It is also showing a more reduced participation than expected in terms of market breadth.

Neutral Signal in Sentiment

The comparison of Z-Scores reveals the disparity between large cap performance (SPY) and the top 1000 stocks by dollar volume (the broad market), equally weighted.

Since early August, the broad market and large caps have been running neck and neck. There is almost no differentiation in performance at the moment, but we suspect the broad market may get the advantage in the next stage — in other words, the Z-Score Divergence will trend toward the lower part of the graph again. “A rising tide that lifts all boats” is bullish.

Bullish Signal in Market Internals Z-Score

Dollar Transaction Volume has fallen dramatically again. The recent consolidation is not attracting buyers or sellers, and we can infer that most investors are content with their positioning. Low dollar volume makes a further advance in the market unlikely at this point, as the liquidity is not there to support much higher prices.

Bearish Signal in Dollar Transaction Volume

5. Trading in the Sigma Portfolio (Live)

After reviewing all of the above factors, it’s time to decide on the actual investing strategy for our real-life portfolio.

The market remains in consolidation mode this week. Our models have barely made any changes. For us, there is no imperative reason to increase or decrease exposure. However, there are a couple of instruments we are watching in particular:

A reversal in bond prices, especially the reaction post CPI data tomorrow (TLT, IEF)

A technical breakdown or reversal and break-out in oil (affecting USO, XLE)

Tactical allocation to the defensive sectors, especially Healthcare (XLV), but also Staples (XLP) and Real Estate (XLRE) — in the event of a BUY signal

As always, we will let the market guide our decisions. As it stands, our allocation is very close to target.

Automated Strategies and Market Outlooks

The Sigma Portfolio (Live)

There are no trades scheduled for today.

Click here to access our own tracker for the Sigma Portfolio and review how each position contributes to the overall exposure profile.

In total, we stand to gain $17.418 by risking $11.639 if our targets are correct. The risk-reward equation has slightly deteriorated from last week’s evaluation, as our positions have gained in P/L terms. For now it’s not necessary to make large adjustments, but we are eyeing an increased position in treasuries, which carry the best risk-reward going forward.