/ August 19 / Weekly Preview

-

Monday:

N/A

---

Tuesday:

Fed Speakers Bostic and Barr

---

Wednesday:

FOMC Minutes

---

Thursday:

Initial Jobless Claims (230K exp.)

S&P Global Manufacturing PMI (49.5 exp.)

S&P Global Services PMI Flash (54 exp.)

---

Friday:

Fed Chair Powell SpeechJackson Hole Symposium

-

Monday:

Estee Lauder EL

Palo Alto Networks PANW

---

Tuesday:

Lowe's LOW

Keysight Technologies KEYS

---

Wednesday:

Target TGT

Macy's M

TJX TJX

Snowflake SNOW

Agilent Technologies A

Zoom Video Communications ZM

---

Thursday:

Advance Auto Parts AAP

Peloton Interactive PTON

Intuit INTU

Ross Stores ROST

Workday WDAY

---

Friday:

N/A

Correction is Over

Last week, we wrote that supply and demand shocks like the “Yen Carry Trade” blow up are temporary issues that cause mechanical selling in the market. These rarely devolve into more extreme affairs, though the risk is ever present in these types of circumstances.

Though the entire drawdown episode was partially predictable from a risk / reward perspective, the speed and conviction with which the rebound rally occured took us entirely by surprise (and not only us, it seems). Now’s as good a time as ever to point out that our automatic systems (Enterprise and Nostromo) were right to be buyers last Tuesday, and we were wrong to be sellers. That puts us in the unenviable posture to play “catch up” with portfolio exposures in the next period.

However, we are certainly not alone in this disposition, as our Volume analysis reveals an unusually low interest from traders in chasing this rally. Dollar Transaction Volume suggests the recovery is a “fake”, while realized volatility (lower panel) remains elevated.

Our Volume analysis is echoed by Goldman Sachs, in their note to investors:

“S&P 500 top book liquidity is currently at $5M. This is down from $26M in July. This is a decline in the worlds equity liquidity instrument of-80% in the last 3 weeks. Top book liquidity hit $3M on Monday, the lowest level since March 2023 (15 months). ETFs represented 43% of the overall market volume on Monday compared to 29% YTD.”

The effect of thin liquidity tends to amplify price movements in any direction, as buyers and sellers are less likely to “meet in the middle”.

As Q2 Earnings Season is mostly behind us, share repurchases will again become a key driver of stock returns in the next period. The “buyback blackout” window which precedes earnings announcements has mostly reopened. Adding to this, pension funds will need to start buying roughly $40 billion a week into September to balance their portfolios for the end of the quarter.

These buybacks are essential, especially in the large caps space, since they continue to provide the bulk of net purchases in the open market. Last week was also full of new repurchase authorizations, with 38 new programs authorized for $15.1 Billion. The surge of buybacks this year is an essential support in the near term and it’s also part of the reason why the correction ended so fast.

Notably, the share repurchase window begins to close again on September 5th.

Technically speaking, SPY is trading near the middle of its expected risk range. Support should come in at around $539 - $545, near the M-Trend level and the 50-DMA. We still expect some momentary weakness to retest support successfully. A small pullback would be the most likely outcome in the near term and provide an optimal entry point. However, the scope of a larger correction now moves closer to the election in November.

Resistance is at $570 (R1), with only the recent all-time-highs standing in the way of more upside.

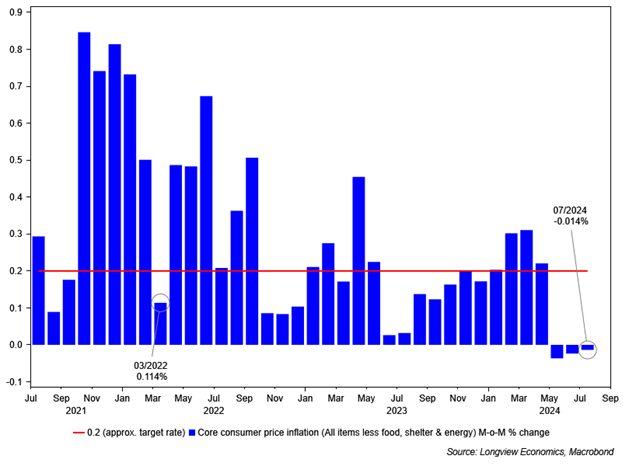

From a fundamental perspective, it was last week’s CPI, PPI and retail sales data which encouraged investors. As expected, CPI and CPI core rose 0.2% for the month (2.9% and 3.2% year-over-year respectively). This pretty much locks the Fed in for a 25 bps rate cut in September (100% priced in). However, if we strip out shelter from the CPI calculations, the Fed may soon begin to worry about deflation.

Core CPI, excluding shelter prices, has shown a negative reading for three consecutive months, a disposition last seen from March to May 2020 during the pandemic. In contrast, the CPI shelter index has increased by 5.1% over the past year and constitutes 70% of the overall year-over-year core CPI measurement.

Despite shelter costs making up 40% of the total CPI, they remain out of sync with independent market data, particularly the Fed’s New Tenant Rent Index. When CPI shelter prices finally align with market trends, this could potentially reduce 40% of CPI toward zero. Consequently, the Federal Reserve will find itself battling deflation next. Rest assured, the Fed’s economists are well aware of the lagging shelter data and understand the flaws inherent in the CPI calculation.

For the bond market, the prospect of deflation is a major upside catalyst. TLT has found bids near S1 support ($96) and our strategies are aiming to increase exposure to treasuries this week.

Our Trading Strategy

Unfortunately, we’ve been reluctant to implement the portfolio allocations suggested by our automatic models. We need to course correct in both stock and bond positions. Lesson learned.

Treasuries can be bought at any point this week, with the major catalyst remaining the Jackson Hole symposium and Jerome Powell’s speech on Friday. A healthy bonds exposure will also help hedge stock market volatility, as a negative correlation between stocks and bonds has emerged.

We’d still like to see a bit of a pullback in equities before pulling the trigger on bids more aggressively. We will have our “shopping list” ready when the time comes.

Ken Griffin, CEO of Citadel Securities has a prescient saying, which is also our guiding principle:

Protecting capital is job one. Profitability is job two.

Signal Sigma PRO members will be notified by Trade Alert of any live portfolio changes (if subscribed). If you’re not on this plan yet, you can get a free trial when you join our Society Forum. If you need any help with your trading strategy (or would like to implement one on your account), feel free to reach out!