/ August 21 / Weekly Preview

-

Monday:

N/A

Tuesday:

N/A

Wednesday:

N/A

Thursday:

Initial Jobless Claims

Durable Goods Orders MoM (0.5% exp.)

Jackson Hole Symposium

Friday:

Fed Chair Powell Speech at Jackson Hole

-

Monday:

Zoom Video Communications ZM

Tuesday:

Toll Brothers TOL

Dick's Sporting Goods DKS

Lowe's LOW

Wednesday:

Nvidia NVDA

Advance Auto Parts AAP

Autodesk ADSK

Foot Locker FL

Snowflake SNOW

Splunk SPLK

Williams-Sonoma WSM

Thursday:

Dollar Tree DLTR

Affirm AFRM

Intuit INTU

Nordstrom JWN

Ulta Beauty ULTA

Workday WDAY

Friday:

N/A

Corrections don’t happen in a straight line either

Over the past week, we’ve seen the market pull back to a fairly large extent, almost hitting our “Correction Target” of $431 on SPY, at the intra-day lows on Friday ($433). However, the market bounced convincingly and managed to close in the green for the most part. This sets us up for a potentially positive week, where a further rally would be likely to build on Friday’s bounce.

We don’t believe price movements last forever in any direction. For now, the market remains very oversold in the short-term and prone to a rally on any piece of good (on “not so bad”) news. However, the nature of the rally would be “reflexive” until proven otherwise and could be used by nimble investors to exit positions, and reduce risk, in anticipation of further corrective action by mid - September.

If we do manage to get a BUY Signal at any point, the plan is to increase our equity risk exposure for a rally into year end. Portfolio Managers and retail investors alike are trying to play “catch up” with index benchmarks, after badly lagging in the first part of the year. For now, the corrective process has been orderly and normal. As long as “nothing breaks”, and the corrective cycle successfully completes, we view the pull-back as healthy and part of the usual stock market volatility.

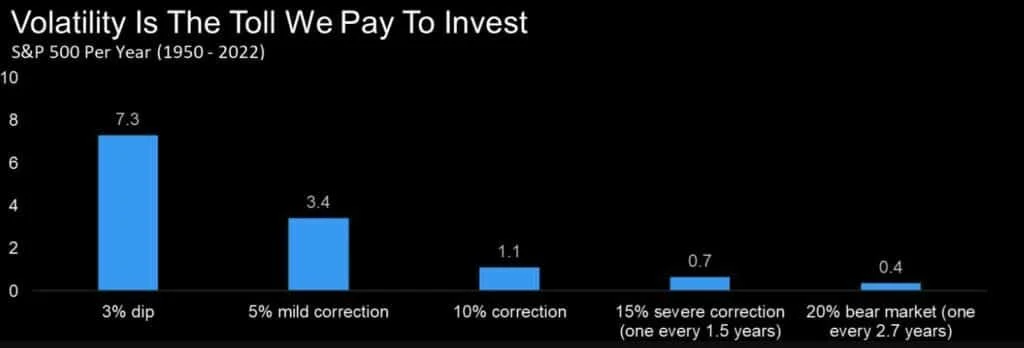

As a reminder, here are the drawdown stats for the S&P 500 since 1950. The drawdown so far for this episode (close to close) is around -4.65%, not exceeding the “mild correction” category below. We’ve already had an -8.37% correction in March.

SPY Analysis

The MACD is now severely oversold and is signaling the velocity of the pullback has been as aggressive as one could expect;

Our best guess is that the market could mount a rally from these interim lows and find resistance at the 50-DMA (being the only technical level directly above). This would not be enough to trigger a BUY on the MACD signal, however.

We also can’t completely exclude a larger correction to the 200-DMA. This scenario would entail a ~10% drawdown, which also falls into the realm of “normality” in every single year. The point we’re trying to make is that unless we get an “all clear” from the market (and our strategies), there is no hurry to buy the dip at this stage.

There are 2 catalysts lining up in the week ahead: NVDA’s earnings on Wednesday and Jerome Powell’s press conference on Friday, at Jackson Hole. We’ll study each of them below.

"I've been covering tech since 1994 and I have never seen an environment where you are so dependent on one company to deliver,"

"AI is really the last pillar of growth and everybody is depending on it. If Nvidia shows weakness, we could be in for quite a substantial correction in the market."

Inge Heydorn, partner at GP Bullhound, which owns both Nvidia and AMD shares

Nvidia’s Earnings Call

NVDA remains the poster child for the A.I. revolution, along with Microsoft. It is probably the first company where A.I. will make a significant impact on the top line, and drive continued revenue growth. The company has been the biggest beneficiary of the rise of ChatGPT and other generative artificial intelligence apps, virtually all of which are powered by its graphics processors. It’s operating model is extremely aggressive and prone to wild fluctuations. Check out the EBITDA and the Operating Model for the following 3 quarters:

Q2 ‘21 - EBITDA of 2.73 B on 6.51 B Revenues

Q2 ‘22 - EBITDA of 0.88 B on 6.70 B Revenues

Q1 ‘23 - EBITDA of 2.52 B on 7.19 B Revenues

If revenues are enjoying consistent growth, the same can’t be said of actual profits. The changes in the bottom line track pretty well with the price chart, as the weakest quarter’s figures (Q2 ‘22) were made public near the stock’s lows.

Versus peers in its industry, NVDA is astronomically valued, at 56 times EV to EBITDA (15.77 being the average). It’s key metrics are not trending any better than rivals’ (declining Sales Growth, Gross Margins and rising Operating Expenses).

The catalyst for the rally has, of course, been the company’s own guidance, and analysts expectations for further upside to that guidance. Wall Street expects the chip company to guide for a rise of about 110% in third-quarter revenue to $12.50 B (from 5.9 B last year). Nvidia has only forecast revenue below estimates once in the past two years.

With shares having tripled in the last 8 months, Nvidia leaves little room for disappointment. We attempt to build a DCF model below to see if the average Analyst Price Target of $513 is justified. We’ll use the following assumptions (try to model it yourself, if you’d like to change these inputs):

Yearly Revenue Growth: 30% (leading up to a 100 B top line in 2027 from 27 B in 2022)

Gross Margin: 61% (versus industry average 51.38%)

Operating Expenses as a percent of Revenue: 32% (versus industry average 28.54%)

EV/EBITDA multiple: 50 (which is heavily debatable, since the closest rival is AMD at 18.86 currently)

We get a $476 Price Target, with a 35% average CAGR.

This is how the figures look like on an adjusted Technical Chart. The stock presents more downside than upside, even given the generous assumptions. Of course, it all hinges on Revenue Growth and resulting valuation. Investors will be looking at sales at Nvidia's data center unit, home to its flagship H100 chip used in AI, to see if the valuation (and revenue growth assumption) can be justified.

Jerome Powell’s Press Conference

In a landmark speech delivered in Jackson Hole, Wyoming, Federal Reserve Chairman Jerome Powell sent shockwaves through financial markets one year ago. Powell made a resolute promise that the U.S. central bank would confront and subdue inflation, regardless of the potential economic repercussions. This announcement had an immediate impact on global financial markets, prompting widespread volatility and a bear market that would extend into October.

12 months later and it’s bonds, not stocks, which are reeling from the policy decisions. While SPY gained 4% in the interim, TLT lost 16%, pushing the Stock-Bonds ratio to a historical deviation. The Federal Reserve has now shifted away from explicit forward guidance and emphasized its reliance on economic data, even during a time when interpreting the data has become more challenging.

This is where we expect things to become murky. As the Fed approaches “optimal policy”, decisions become tougher. Core CPI is still much higher than the Fed’s annual target of 2%.

The calculation of inflation data is affected by several quirks, adding complexity to the outlook. Headline inflation numbers are derived from comparing current prices with those from the corresponding period in the previous year. As price growth picked up speed during the spring and summer of 2022, this year's inflation figures indicated a significant slowdown. However, as we move beyond the one-year anniversary of the peak inflation reading in July 2022, the year-ago comparisons will no longer appear as favorable. Consequently, inflation rates are likely to remain relatively stable or move sideways for the next few months. This explains Neel Kashkari’s statement:

“Are we done raising rates? I’m not ready to say that we’re done.”

Our Trading Strategy

With most asset classes very oversold in the near term (and the U.S. Dollar exceedingly overbought), we wouldn’t be surprised to witness a reflexive bounce. Both catalysts that we have covered could lead to a temporary rise in prices, provided they are not “catastrophic”.

For the moment, the short term opportunity is to reduce risk into the bounce. If we get a confirmation that the correction is over, we will start adding to equity risk.

Signal Sigma PRO members will be notified by Trade Alert of any portfolio changes (if subscribed). If you’re not on this plan yet, you can get a free trial when you join our Society Forum.