Weekly Preview / November 28

Notable Events on our Weekly Watchlist:

Monday: N/A

Earnings: N/A

Tuesday: Consumer Confidence

Earnings: INTU, WDAY

Wednesday: EU Inflation, ADP Employment Change, JOLTS Job Openings, Powell Speech

Earnings: NTNX, OKTA, CRM, SNOW

Thursday: Personal Income / Spending

Earnings: DG, ULTA

Friday: Non-Farm Payrolls, Unemployment Rate

Earnings: CBRL

ETFs to watch: QQQ, IVW, TLT

Bullish bias persists in light trading volume

There was little to take note of in last week’s trading. Volume was VERY light, and the price action mostly consolidated, as expected. As it stands right now, there is little to add to our analysis. The risk range for SPY has widened a bit however:

Resistance: 413 (up from 412 last week)

Support: 386 (down from 387 last week)

Furthermore, the main index-tracking ETF is being pressured between short term support at the 20-day Moving Average at 389 and strong overhead resistance just above, at the 200-day Moving Average (404). While not part of our analysis methodology, these moving averages offer psychological pivot points, as many traders follow them.

With the bullish bias still intact, it would not be surprising to find SPY trading above the 200-day Average, but it would also not mean anything special either. The trading week is back-loaded, with Wednesday and Friday set to be the most important days ahead. Here’s the technical breakdown:

SPY Analysis

The short-term MACD indicator is still positive, but we are noticing signs of fatigue in the current rally. The first 2 weeks of December tend to be seasonally weaker, as mutual funds enter distribution season and need to make sales in order to meet outflow obligations.

The Market Internals / Volume reading has continued dropping. This is partially related to the light trading of last week, but we also suspect some of the drop is related to buyers simply running out of steam absent a major catalyst for now. As per usual for this year, the only catalyst that counts is inflation and the Fed.

Traders seem to price in a positive scenario, pushing near-term price action to more extended extremes, which have previously been great opportunities to reduce equity exposure and raise cash. A lot of this pricing has to do with an expected slowdown in the Fed hiking cycle, and the assumption that the US will avoid a recession in 2023.

Is a recession avoidable in 2023?

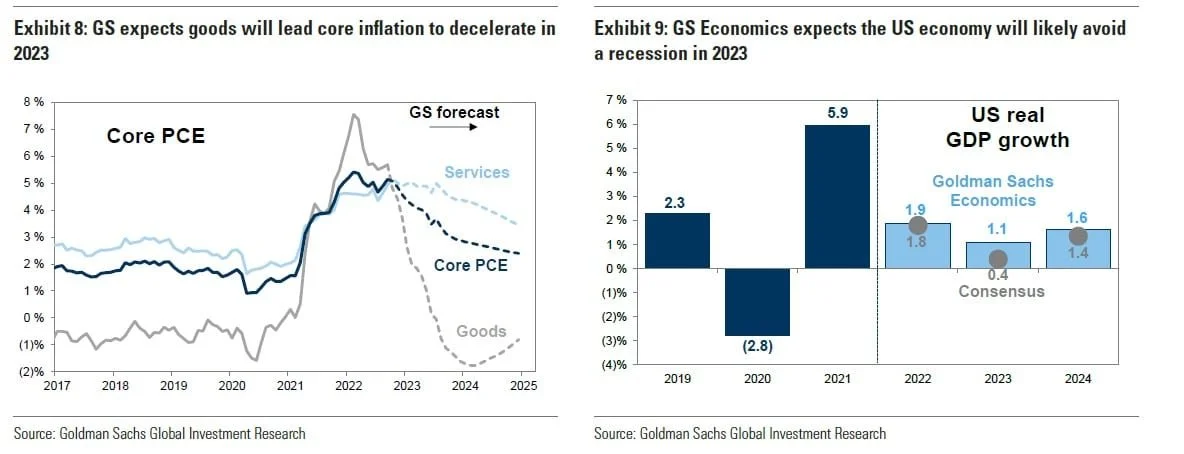

Economists from Goldman Sachs (and indeed more bullishly biased traders) think so. Recently, they published the following outlook:

“While it is too early to call for a Fed pivot based on a few inflation readings that remain well above the Fed’s 2% target, our economists forecast steady declines in core PCE in 2023. They expect goods deflation and services disinflation will drive core PCE from 5% today to 3% at the end of next year (Exhibit 8). Progress in corralling inflation means the Fed will raise rates by 50 bp in December, followed by 25 bp hikes in February, March, and May that will lift the Fed funds rate to 5.0%-5.25%. The policy rate will stay high to keep growth below trend.

Importantly, under the soft landing scenario, our economists forecast below-trend GDP growth will be accompanied by just a 1/2 point increase in the unemployment rate to 4.1%, and the US economy will avoid recession in 2023.”

Under Goldman’s assumptions, a “soft landing” scenario would simply imply no growth for 2023 in terms of S&P500 EPS. In the case of a recession, an 11% decline in EPS is penciled in, as per the following table:

The possibility that the US will avoid a recession in 2023 is echoed by the Atlanta Fed GDPNow estimate for Q4 2023 - now at 4.3% compared with a consensus view of about 0.5%.

While the possibility of a a “soft landing” scenario does indeed exist, it it not necessarily the most probable scenario. Our job as investors is to weigh every piece of information accordingly and form a reasonable investment thesis for the future.

While the probability of a recession in 2023 is much more significant than Goldman (and the Atlanta Fed estimate) predict, there is one significant fly in the ointment for the bears: EVERYBODY IS EXPECTING A RECESSION IN 2023. This has us a bit bothered, because in the equity market, whenever “everybody agrees” on something, it’s usually already priced in, or something else tends to happen.

Let’s plot Goldman’s assumptions for SPY using our improved Technical Analysis Instrument and get some insight into the near-term trading range for the market.

The Soft Landing

Implies a near 0% EPS growth rate (and similar CAGR setting), with a 400 Price Target.

This scenario implies equities are fairly valued at the moment, with upside only to 432 (if more optimism takes hold) and downside to 370 (on more bearish supply and demand dynamics). $30 either way does not make for an attractive risk-reward at this point.

The Hard Landing

Implies a negative EPS Growth of 11% and a Price Target of 315 at the lower end of the projection (341 at the midpoint).

Intuitively, this scenario looks more probable at this point. The market seems to trade at the top end of the technical channel (near 408 with these assumptions), with indicators pushing more overbought extremes. Very little upside is left, with near-term technical downside to 350. If the market does indeed follow this path, a range-trading approach looks like our best bet to profit.

Takeaway

No one can predict the future path of financial markets. Our job as portfolio managers is to take account of every piece of available information and make informed decisions for our clients and our portfolio. While many participants (especially in the bond market) are pretty much convinced a recession will occur in 2023, some investors are already looking “beyond” the downturn. This explains most of the bullish views from the present environment.

If we discount the high probability of a recession (about 60-70% in our opinion) with the risk-reward available today in the “no recession” scenario, it leaves us with little reason to initiate new long positions - equities are fairly priced, not under-priced. A “better bet” is to take the bearish side, and initiate short positions at this juncture, up to 30% of portfolio value.

Overall, the treasury market looks much more attractive, and I believe it will be the leading asset class of 2023. We must be patient, however, because short term, treasuries are extended as well from a technical point of view.

We will take profits in our Energy positions and reduce the position in commodities this week. XLE has not followed the decline in oil, and this performance differential might be closed to the detriment of our portfolio. Other than that, there is no directional bet that we are willing to take a risk on. We need to simply let the market tell us what comes next. Until that, patience is the key-word.

Andrei Sota

XLE vs USO Instrument Comparison