The US Dollar Special Report / August 17

As the Dollar Throws Its Weight Around, the World Absorbs the Shock

In mid-July, the dollar saw a nearly 14% jump from its May 2021 low, reaching its highest level in two decades. For a short time, the dollar was even with the Euro, causing chaos on a global scale. Since much of the global monetary landscape revolves around the dollar, governments, multinational companies, and people around the world are feeling the squeeze from our currency’s fluctuations. In the last couple of weeks, the dollar has cooled by 1.58% thanks to positive signs of slowing inflation, but things might take a while to fully recover. UUP is the ETF that tracks the USD against a basket of world currencies via USDX future contracts. We compare its 2 year performance (white) vs a portfolio of equal weight asset classes (SPY, TLT, GLD, DBC). We find that holding UUP for the past 2 years has provided better returns than a combination of asset classes.

USD (white) vs SPY, TLT, GLD, DBC - equal weight (orange)

What Made the Dollar Fluctuate?

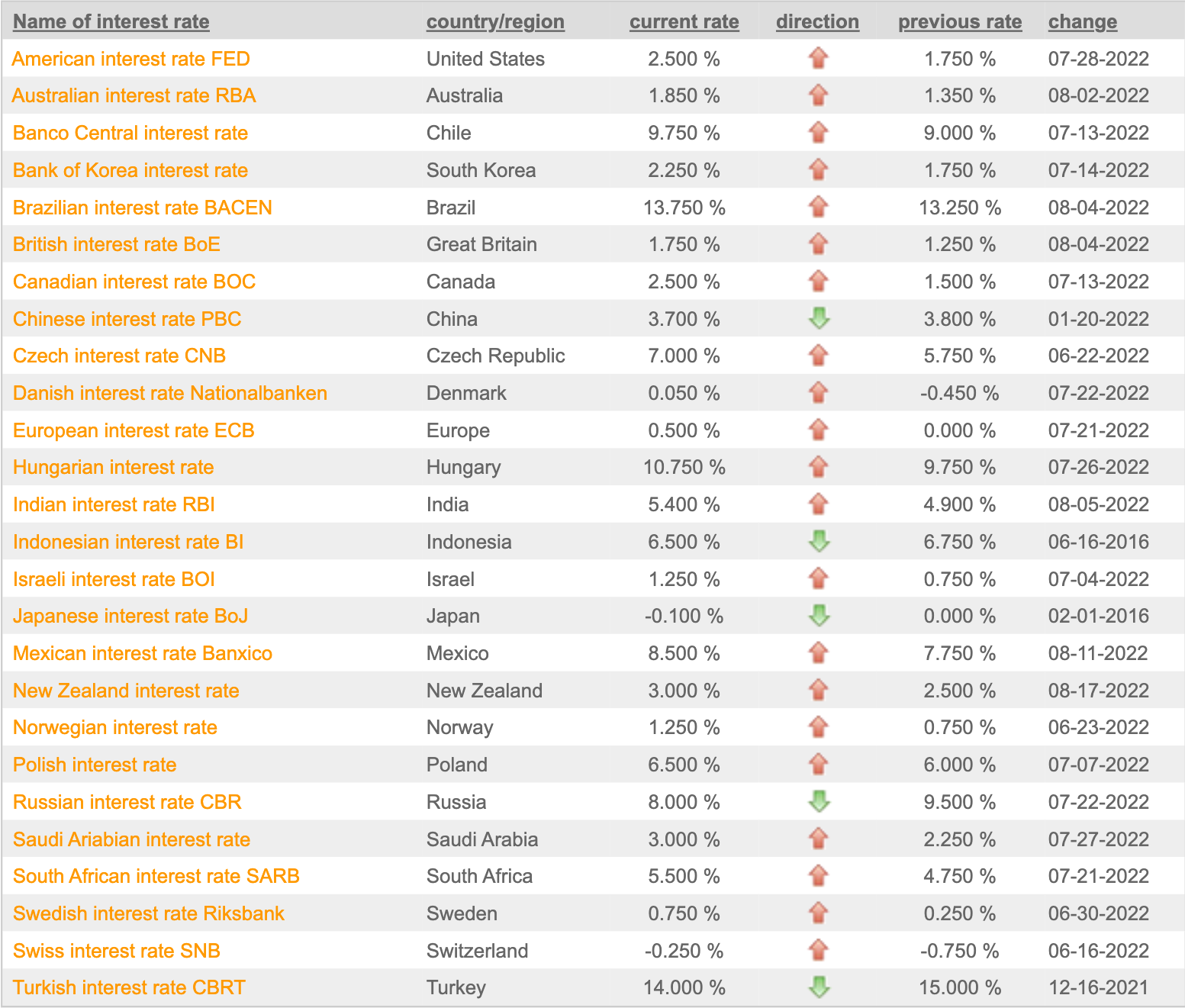

Facing post-pandemic disruptions, record inflation, and reeling from a war in Europe, the US economy has had its fair share of obstacles this year. To some, it might seem shocking that the dollar pulled ahead so quickly and effortlessly, but in reality, the dollar’s strength is largely in part due to the fact that the rest of the world is dealing with similar struggles. The Federal Reserve responded swiftly and aggressively, increasing interest rates in an attempt to curb inflation; this strong response positioned the US more favorably than other countries that have been slower to react to record inflation levels globally.

30 Day Risk Free Trial

Try our Research Plan and see if it’s right for you.

Source: https://www.global-rates.com

How the Dollar Impacts Global Trade

Since the US is a major importer of products, there are some benefits to a stronger dollar for consumers; international products will be cheaper, helping to curb inflation in the US even more. A study by the Federal Reserve Bank of Cleveland estimated that a 1% rise in the dollar pushes non-petroleum import prices down by 0.3% over six months, signaling net positives for the US economy from a consumer perspective.

On the other side of the equation, products exported by the US will be less competitive in international markets because they are more expensive for consumers in other countries. This could lead to a massive decrease in sales for companies that do business abroad, further exacerbating the headwinds that those same companies feel from exchange rate woes.

Multinational Companies Feel the Pain

Companies based outside of the US will see an upside thanks to the dollar’s strength, but US companies that conduct large amounts of business internationally are facing massive exchange rate headwinds. A global markets strategist at eToro, Ben Laidler, estimates that S&P500 companies will see a 5% reduction in earnings growth – which is equivalent to about $100 billion – solely because of the dollar’s rise.

Unfortunately for companies that conduct business abroad, the records set by the dollar came just in time for Q2 earnings season. In 2021, S&P500 companies brought in 29% of their sales from outside the US, but some sectors, such as technology, see international sales as a much larger portion of their overall revenue. Goldman Sachs estimated that tech companies bring in as much as 59% of sales from abroad, making organizations like Netflix, Microsoft, and Apple more vulnerable to exchange rate headwinds. Microsoft generates half of its profits from other countries, with foreign exchange rates shaving $302 million from sales last quarter. The company is expecting these rates to further impact next quarter by eroding $460 million in sales.

Market Reaction

Dollar fluctuations make managing a large, international portfolio challenging. According to Goldman’s indices of S&P 500 companies, those with a large international presence are down 19.6% this year, more than double in comparison to the domestically-weighted counterpart, which is only down 9.1%. Jonathan Golub, head of US equities at Credit Suisse, noted that though Q2 earnings showed a 10% increase compared to last year, it would have been closer to 12% without the challenges coming from exchange rate fluctuations.

Domestic Exposure performing better than International Exposure

Goldman Sachs / FT

Developed Nations Struggle to Keep Up

In Europe, countries rocked by rising fuel prices amidst an energy crisis are reeling; as the euro recovers from parity with the dollar, the European Central Bank struggles to keep up with raising interest rates at the same rate as the Federal Reserve. The yen also tumbled to record lows this year and is working through a recovery now.

Developed nations all over the world are facing the same challenges: record levels of inflation, pandemic recovery, climate change, and rising geopolitical tensions. Fighting against common issues, central banks of G20 countries are all tightening monetary policy at the same time. It’s unclear whether this tightening will tip the scales of a global recession or help pave the way toward recovery, but either way, it’s a necessary step for every country at this point.

Emerging Markets Hit Even Harder

Since 90% of the world’s currency trades involve the dollar as one of the currencies being traded, there is not a country on earth that will not be impacted by rapid changes in the value of the dollar. Emerging markets that borrowed a lot of money when US interest rates were at 0% are now facing bigger repayment bills while the currency of these countries is being devalued. The World Bank predicts that nearly 60% of low-income countries are vulnerable to debt distress or are already in it.

Sri Lanka and Argentina are two countries that seem to be teetering on collapse, and the rise in the value of the dollar greatly exacerbated their problems. Since dollar debt represents a large portion of these countries’ gross domestic product, its rise in value is increasingly difficult to overcome. However, countries like Angola, Uruguay, and Brazil, which are exporters of oil, food, and agricultural commodities respectively, have found insulation from exchange rates thanks to the rising costs of energy and food.

Understanding the Ruble’s Reaction

One of the best-performing currencies against the dollar has been the Russian ruble, despite the country waging war in Ukraine. High costs of energy and gas, and much of Europe’s dependence on the country for these resources, have helped insulate the Russian economy from taking as much of a hit as expected. Though the Russian government had to shut down its financial system to the outside world, the country is getting by and signaling strategic moves to separate itself from the US even further.

After hitting a record low of 121.53 to the dollar in March, the ruble skyrocketed to a peak of 50.01 in June. However, in July, the ruble dropped 16%, becoming one of the worst performers against the dollar. Amid western sanctions, demand in Russia for the yuan has shot up, raising questions by foreign policy experts about China and Russia moving to be completely independent from the US, which could have major long-term implications.

RUB vs USD 1 Year Chart (xe.com)

Get market updates in your mailbox as soon as they become available. Sign Up to our Press Account.

CONCLUSION

The Future of the Dollar

Inflation showed signs of slowing in July, with consumer prices seeing an 8.5% year-over-year increase as opposed to the 9.1% increase in June. Though it’s not clear that inflation has peaked, the chances that the Fed raises interest rates by .75% have fallen, leading to a decrease in the value of the dollar. Though major currencies like the yen, euro, and Australian dollar have seen some recovery, many analysts expect the dollar to maintain strength throughout 2022. For investors, hedging with commodity-based investments and US-based companies that conduct most business domestically are two great ways to weather the turbulence.

Jerica Kingsbury

Disclosures / Disclaimers: This is not a solicitation to buy, sell, or otherwise transact any stock or its derivatives. Nor should it be construed as an endorsement of any particular investment or opinion of the stock’s current or future price. To be clear, I do not encourage or recommend for anyone to follow my lead on this or any other stocks, since I may enter, exit, or reverse a position at any time without notice, regardless of the facts or perceived implications of this article.

I am not a financial advisor. Nor am I providing any recommendations, price targets, or opinions about valuation regarding the companies discussed herein. Any disclosures regarding my holdings are true as of the time this article is written, but subject change without notice. I frequently trade my positions, often on an intraday basis. Thus, it is possible that I might be buying and/or selling the securities mentioned herein and/or its derivative at any time, regardless of (and possibly contrary to) the content of this article.

I undertake no responsibility to update my disclosures and they may therefore be inaccurate thereafter. Likewise, any opinions are as of the date of publication, and are subject to change without notice and may not be updated. I believe that the sources of information I use are accurate but there can be no assurance that they are. All investments carry the risk of loss and the securities mentioned herein may entail a high level of risk. Investors considering an investment should perform their own research and consult with a qualified investment professional.

I wrote this article myself, and it expresses my own opinions. I am receiving no compensation for it, nor do I have a business relationship with any company whose stock is mentioned in this article. The information in this article is for informational purposes only and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

The primary purpose of this blog/forum is to attract new contacts with professional industry expertise to share research and receive feedback (confirmation / refutation) regarding my investment theses.