Signal Sigma Strategy Results Q2 2022

Observations on Signal Sigma Strategies quarterly performance

Let’s get one thing out of the way - in a decidedly bearish market environment, where CASH is the best performing asset class, our long only strategies cannot be profitable. The best outcome for these models is to preserve capital, mitigate risk, and outperform by declining less than the overall market. When the time is right, we will use the (very large) cash cushion to invest accordingly. Systemic models need momentum in order to generate profits, and momentum has only been to the downside. In that sense, stop orders and sell signals have done an excellent job in protecting our funds. Armed with this perspective, let’s dig in to the Q2 performance numbers (April 1 - June 30).

SPY -16.71%

TLT -13.23%

DBC +1.56%

GLD -6.15%

ETFs that represent the main asset classes have done poorly as a group. I will reiterate a chart that I’ve often used in our Portfolio Rebalance articles to make the point.

Cash (white) is simply King, as performance is now almost up to par with all asset classes combined (orange)

Strategy Returns

Our models aim to blend asset classes that “work” into a portfolio that returns a smooth, upward sloping equity curve. The strategies differ in allocation method and aggressiveness, with good risk-reward characteristics for each. Drawdowns are limited by using a volatility parity system and eliminating asset classes that violate stop losses. Right now, 3 out of 5 asset classes are deemed un-investible (Equities, Treasuries, Gold). Let’s review our models performance during the quarter, in one of the worst environments to be long-only in:

Enterprise (least risky strategy): -4.34%

Nostromo (moderate risk): -8.31%

Horizon (high risk): -13.57%

As you can see, all of our strategies managed to outperform a benchmark 50% equities - 50% treasuries portfolio.

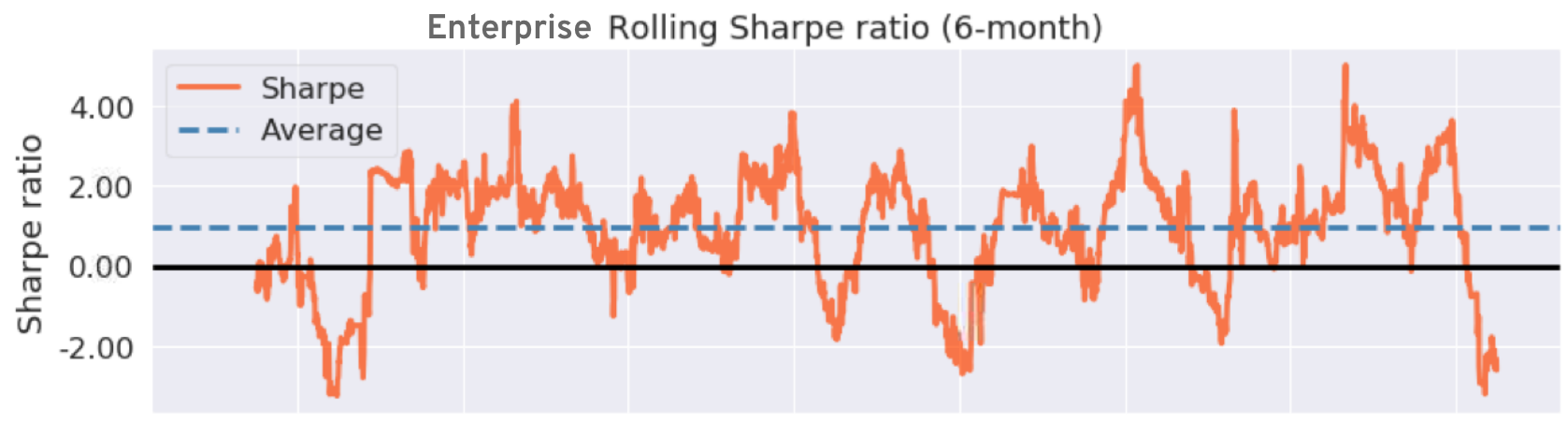

Sharpe Ratio

From a 6-month rolling sharpe perspective, we are noticing all algorithms making relative lows. Previously, these lows in relative returns have marked excellent opportunities to deploy funds into the model’s management. One caveat - Horizon is a strategy backtested since 2010 (the earliest we have fundamental stock data) so the sharpe ratio new lows make sense.

Max Drawdown (Underwater Plot)

The Max Drawdown characteristics for all models are also testing the lower bounds. Horizon is again the exception, since it has not been backtested during the Great Financial Crisis. For this model, a bear market is a novelty, but so far it is performing within the bounds of a high-risk, high-reward strategy. Enterprise is the model that is looking best from this perspective, and is clearly showing why it is the centerpiece of Signal Sigma strategies.

Conclusion

Q2 performance has been lacking, and there’s no denying that we wished for a better showing, especially given the fact that this is the first public quarter for Signal Sigma. We are confident, however, that the strategies contain solid investment principles that will provide long term outperformance. In times of distress and drawdown, outperformance is characterized by the preservation of capital. That is our greatest priority at this stage.

Andrei Sota