/ June 26 / Weekly Preview

-

Monday:

N/A

Tuesday:

Durable Goods Orders (-1% exp.)

Wednesday:

Fed Chair Powell’s Speech

Thursday:

Fed Chair Powell’s Speech

Initial / Continuing Jobless Claims

Friday:

Personal Income / Spending

Core PCE Index

-

Monday:

Carnival CCL

Tuesday:

Walgreens Boots Alliance WBA

Jefferies JEF

Wednesday:

Micron Technology MU

General Mills GIS

BlackBerry BB

Thursday:

Nike NKE

McCormick MKC

Paychex PAYX

Progress Software PRGS

Friday:

Constellation Brands STZ

Administrative Notice: This week, our “Weekly Preview” newsletter will include elements from the “Portfolio Rebalance” article, which is temporarily on pause until the platform re-launch.

Has sentiment topped?

Last week, equity markets took a respite from the breakneck buying frenzy that started in mid-March. Besides grossly overbought and extended deviations, some commentators attributed the correction to weak economic data that continues to suggest a recession is around the corner. The absolute collapse in both implied and realized volatility suggests investors have become complacent to risks and sets us up for a rather poor short-term outcome. Such low levels of volatility have almost always preceded 5-10% corrections in bull and bear markets alike. The historic divergence between SPY’s performance and the broad market continues to act as a nasty hangover. And Jerome Powell’s comments suggest that more rate hikes are likely coming. We unpack everything below, starting with SPY’s Technical Analysis.

SPY has been able to hold support at the $431 R1 Level, despite last week’s correction. However, we view this support as rather frail. The MACD Signal will trigger a SELL from a very high reading (similar to December, when the market experienced a 5% drop), suggesting that this level will be breached. Our automated models are looking to reduce equity exposure on the trigger, and other similar strategies will also sell (Viking Analytics runs a model that will cut exposure around $426 for example).

Our technical model suggests SPY will find strong bids around the $418 mark.

SPY Analysis

The MACD looks to be triggering a SELL from a rather high reading, suggesting there is scope for a more sizable decline

From a sentiment perspective, we note that the market briefly touched “Extreme Greed” and pulled back instantly. Sentiment is now contained in the usual (non-extreme) range. As a contrarian indicator, we can’t derive any meaningful insights from the present reading, although there are 2 things worth mentioning:

once the market reaches an extreme, it usually maintains that level for 1 or 2 weeks, pushing in either direction; it’s uncommon to see such an abrupt reversal;

the last time we have recorded any “Extreme” reading was in March; fluctuations are usually more common (which brings us to the next point)

Volatility is at a record low (even when extending the timeframe to the last 4 years). The spread between implied and realized vol is barely positive, suggesting downside protection is not in demand. While not in itself a problem, conditions are very similar to those that precede vol spikes and market drawdowns.

Such a tame trading environment does not exist in a vacuum, and the logical reason (or should we say “mechanic”) behind low volatility is high volume. Dollar transaction volume has been on a tear recently, with liquidity marking a new high. Notably, rising equity prices on strong volume is bullish.

We ran a screener to determine the S&P500 companies that experienced a surge in trading volume (5 Days vs 90 Days) and the results are not quite what we were expecting. There were a couple of “usual suspects” like tech giants ADBE and ORCL, but we note plenty of industrial companies as well. These look to us like names that investors are looking to accumulate under selling pressure. (Col. A is 5d Volume, Col. B is 90d Volume, Col. C is difference). The selection of names strikes us as healthy, since there is limited accumulation in tech.

Looking at the short and long term Sectors Performance reveals an environment where Tech (XLK), Consumer Discretionary (XLY) and Communications (XLC) continue to show extreme deviations to the upside. Meanwhile, Energy (XLE), Utilities (XLU), Financials (XLF) and Basic Materials (XLB) remain unloved and could be favoured in a “rotation” trade. It is this type of price action that could support SPY, if and when the current leadership fades.

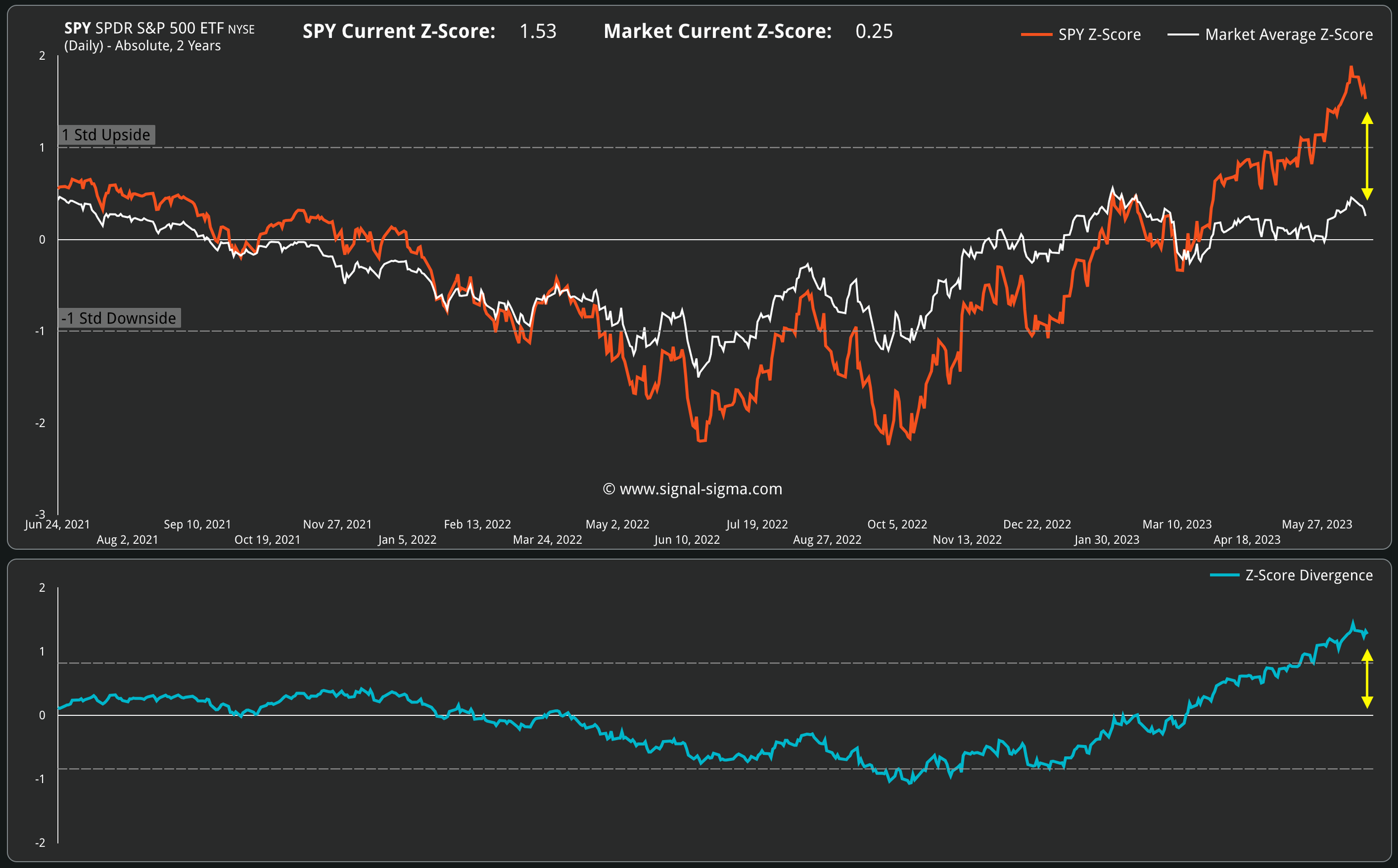

Comparing SPY’s Z-Score (deviation from the trend) to the average Z-Score of a stock in the market points to a historic divergence. Rarely has this level of performance differential existed. When this gap closes, capital will flow from the current out-performers (AAPL, MSFT, NVDA, GOOG, AMZN) to “the rest”. It is this rotation that we are positioned for, currently.

The Fed’s take

Rising stock markets tend to shore up consumer confidence, which, in turn, supports spending on goods and services. This spending, of course, supports inflation, which, according to Chair Powell (and the FOMC) is still a problem. He noted the following, during last week’s Congressional testimony:

“Inflation pressures continue to run high, and the process of getting inflation back down to 2 percent has a long way to go. Nearly all [officials] expect that it will be appropriate to raise interest rates somewhat further by the end of the year.”

As any economist will understand, reducing inflation requires slower economic growth and “softer” labor markets. This will also translate into lower corporate earnings, as overall spending contracts. We use weekly aggregated market fundamentals measures for companies in the S&P500 to pinpoint where we are in the economic cycle.

Notably, while Revenue Growth, Gross and Net Margins have normalized, EPS has not. Earnings have come down slightly, but there has been no dramatic correction yet - EPS is clearly running above trend. The Fed’s ultimate goal is to put a definite stop to the inflation phenomenon and avoid another flare-up similar to the 1970’s.

With EPS still strong and no signs of cracks in the labor market, our fear is that they can afford to keep rates higher for now. This will inevitably act as a “ceiling” to the equity market performance, outside of supply and demand swings.

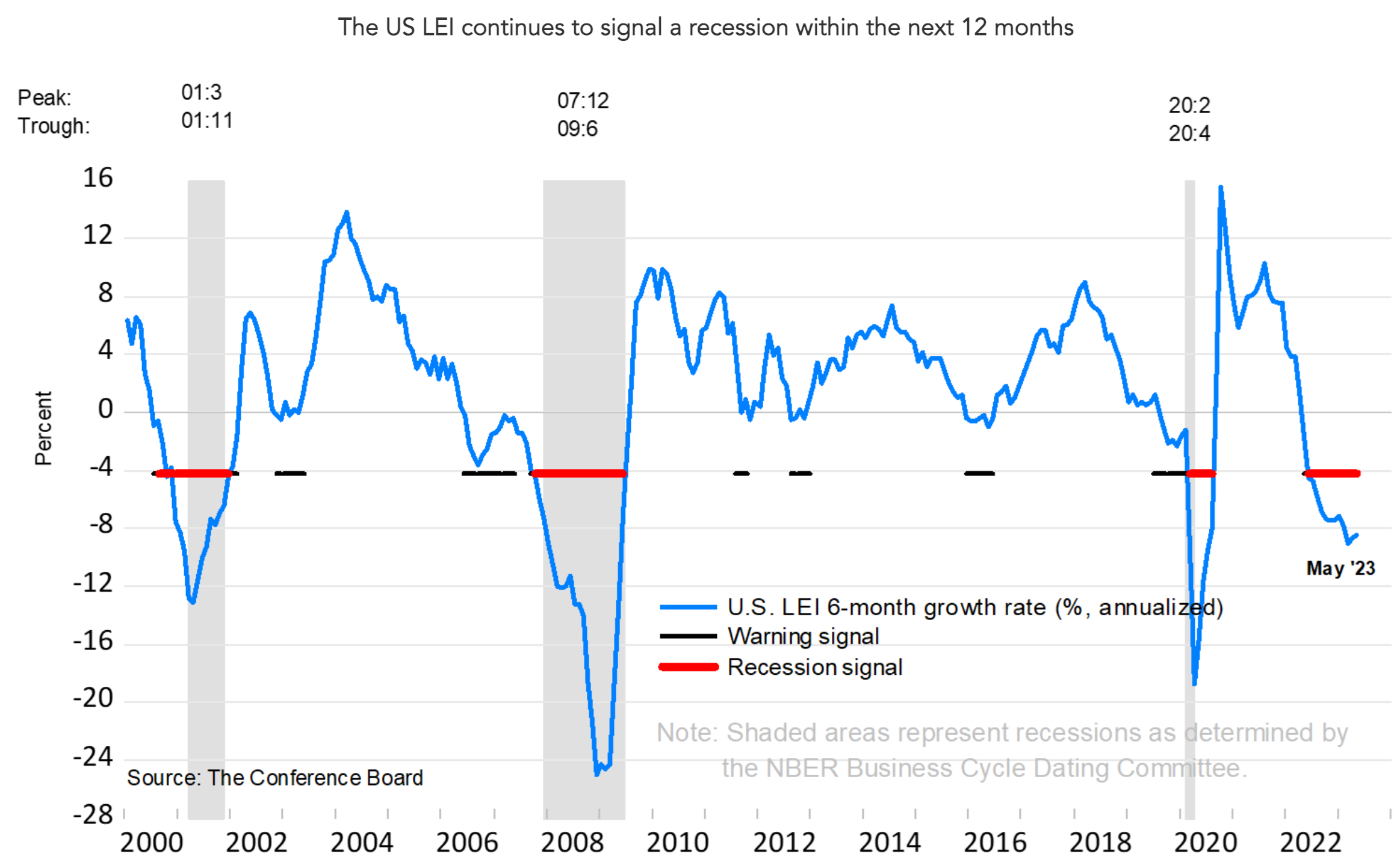

Meanwhile, the US Leading Economic Index (LEI) still points to a recession in the next 12 months. The LEI is one of the most robust fundamental indicators out there:

“The 6-month rate of change (ROC) in the Conference Boards Leading Economic Index (LEI) further supports that recession warning from the ISM composite index. Since 1967, a recession has occurred when the 6-month ROC fell below -3%. This indicator has the most infallible record of all the recession indicators we track.”

“The US Leading Index has declined in each of the last fourteen months and continues to point to weaker economic activity ahead. Rising interest rates paired with persistent inflation will continue to further dampen economic activity. While we revised our Q2 GDP forecast from negative to slight growth, we project that the US economy will contract over the Q3 2023 to Q1 2024 period. The recession likely will be due to continued tightness in monetary policy and lower government spending.”

Our Trading Strategy

What do we make of all the data? There seems to be a slow-motion head-on collision between the Fed and investors currently. This contest only has one winner (hint: it’s not investors). The only “peaceful” resolution would occur if the Fed reverses rate hikes in the face of decreased inflation that does not cause inflation… an unlikely scenario.

Yet the bullish technical price action is undeniable, at the index level. This market trades like it’s coming out of a bear market (not a bear-market rally). This is the kind of backdrop where dips should be used opportunistically to add equity risk exposure to portfolios. However, it does depend on one’s previous stance:

If an investor is under-allocated to equity risk, adding exposure on a pullback makes sense

If an investor has already been fully allocated and benefited from this rally, it’s time to lock in profits now and look for opportunities later to deploy dry powder

We are in the second category, fully allocated. It is therefore our strategy to sell first, and look for opportunities later (especially in sectors that could benefit from a rotation trade).

In any case, tightening up stop losses and selling laggards are actionable steps that should benefit both investor categories at this juncture. We’ll keep you updated with our trading throughout the week.

Bonus chart: all 2911 US stocks in our database combined. The performance is not exactly impressive, is it?