Weekly Preview / March 20

Notable Events on our Weekly Watchlist:

Monday: N/A

Earnings: FL

Tuesday: N/A

Earnings: NKE, GME

Wednesday: UK Inflation, Fed Interest Rate Decision

Earnings: CHWY

Thursday: Initial Claims

Earnings: DRI, ACM, AUY

Friday: N/A

Earnings: N/A

ETFs to watch: SPY, TLT

The Fed has to choose - financial stability or inflation

Developments in the banking sector have continued this past week, giving equity investors no respite from market-moving headlines. Following a brief rebound, the market has now confirmed the break of key support: M-Trend @ $394 on SPY is now resistance.

However, in the short term, many stocks are fairly oversold. A technical bounce on “not as bad as feared” type of news (especially surrounding the Fed decision on Wednesday) would certainly set up a retest of the $394 - $402 resistance area. Expect talks of a “pivot” in the face of financial distress to give a lift to risk assets this week. Any rally would be short lived in our view, since there is a lot of overhead trend-line and 50-DMA resistance right above.

SPY Analysis

Triggering a MACD BUY Signal would not be surprising at this stage - the signal has traversed well into the lower bound.

The day-to-day volatility and financial media headlines hide the fact that the market has traded in this very same range 2 years ago. In other words, for the past 24 months, SPY has been doing… not much. Financial stability has not been an issue. When analyzing the markets, the Fed can take a similar view (and use an even longer term frame) in order to assess the “damage” from their tightening campaign.

However, going forward, they are most likely facing a tougher choice. Just 2 weeks ago, Jerome Powell was testifying before the Senate Banking Committee, using some very hawkish rhetoric:

“If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes.The latest economic data have come in stronger than expected, suggesting that the ultimate interest rate level is likely to be higher than anticipated.”

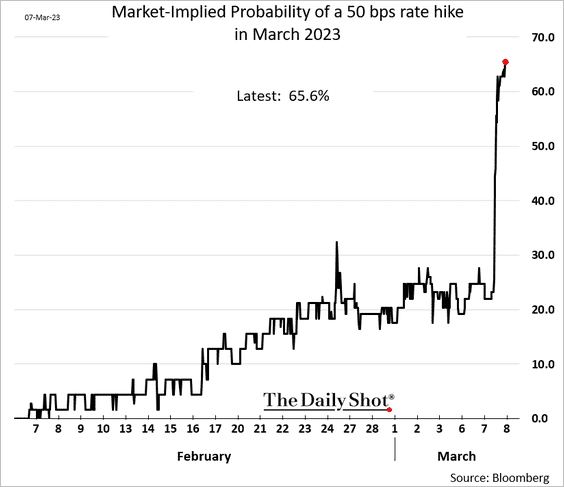

This statement led to an increase in the odds for a 0.50% hike at the March FOMC meeting.

March 07, implied odds for 50bps rate hike

Just one week after that testimony, the banking industry came under pressure, with 3 relatively large U.S. lenders in need of rescue (SVB, Silvergate, First Republic). European banks followed suit, with the next domino to fall being Credit Suisse, which required state intervention and a forced buy-out in order to prevent its collapse.

Odds for a 50bps rate hike quickly plummeted, with safe-haven asset classes rallying hard.

Now, futures markets only see a 33% chance that the Fed will go ahead with a final rate hike this Wednesday and they see up to a percentage point of rate cuts by yearend. The complete turnabout is unsurprising, given the fact that it was always “financial in-stability” that would trigger a Fed pivot.

However, while a Fed pivot wold solve any kind of financial distress in the banking sector, it would also bring about…

… more inflation.

The latest inflation print was not particularly optimistic. Sticky inflation is not budging, despite the Fed’s efforts to cool the economy. Coming in at 6.59% in February, up from January’s 6.55% level, sticky inflation looks unaffected by the central bank’s rate hike campaign.

The sticky-price CPI includes many service-based categories, including medical services, education, and personal care services, as well as most of the housing categories which, by their very nature, change price infrequently. Along with Core CPI, sticky inflation is a better measure of the real inflation phenomena, and how this translates into the larger public’s perception and psychology.

The Fed is very concerned about a 1970’s like resurgence in inflation and a psychological expectation taking root the mind of the population. What they do not want to let happen is a potential hyperinflation spiral which would need much more drastic measures in order to tone down.

Therefore, they are unlikely to pause at this week’s meeting, despite the crisis in the financial sector. Throughout history, whenever a central bank paused its rate hike campaign, it would not be able to resume that campaign again, without first taking interest rates lower. In the event of a “pause”, the market would be right to interpret the move as a “pivot” down the line.

Of course, with ever higher rates comes the risk of “something breaking” in the economy. Bonds and safe havens have already sniffed out that scenario. Shown below, TLT (Long Term Treasuries), GLD (Gold) and even BTC-USD (Bitcoin) in rally mode. There was also a notable performance pickup in long-term assets like giant, profitable, tech companies, as well. Capital is looking for places to hide, and liquidity of an asset comes top of mind.

The “Flight to Safety” trade

For the moment, all of these asset classes seem fairly overbought in the short term. Nevertheless, the Fed is facing a tough choice and soon enough we’ll get to see their resolve. There does not seem to be any scenario where they tame inflation with no economic damage whatsoever.

The most likely scenario remains a recession which will give the green light for the Fed to ease. This will not be shareholder friendly.

Takeaway

During the past week, we deployed a hedge position and reduced risk in economically sensitive stocks. As it stands right now, we are content with positioning and we’ll be waiting until the “smoke clears” form the banking crisis. There is no telling what else is at risk of contagion.

On the Market Internals Instrument, we are seeing a huge spike in volume, as the sheer size of transactions confirms the recent downward trend. This is not what we would like to see in the event of a rebound. Volatility has remained elevated.

The number of stocks managing to hold their 200-DMA’s is breaking down.

But the market is oversold enough to elicit a technical bounce - especially if the Fed comes out with more dovish language.

The overall trend for equities remains lower, for now. Bonds and Gold have outperformed, so a pullback would not be unexpected. We are in a “mean-reversion” type trading environment, where extremes make for good entry / exit points. However, while trading these might net us some profits, the main objective remains capital preservation during these uncertain times.